Half-year 2026 update, reflections on +55%

My best half-year yet (but only just)

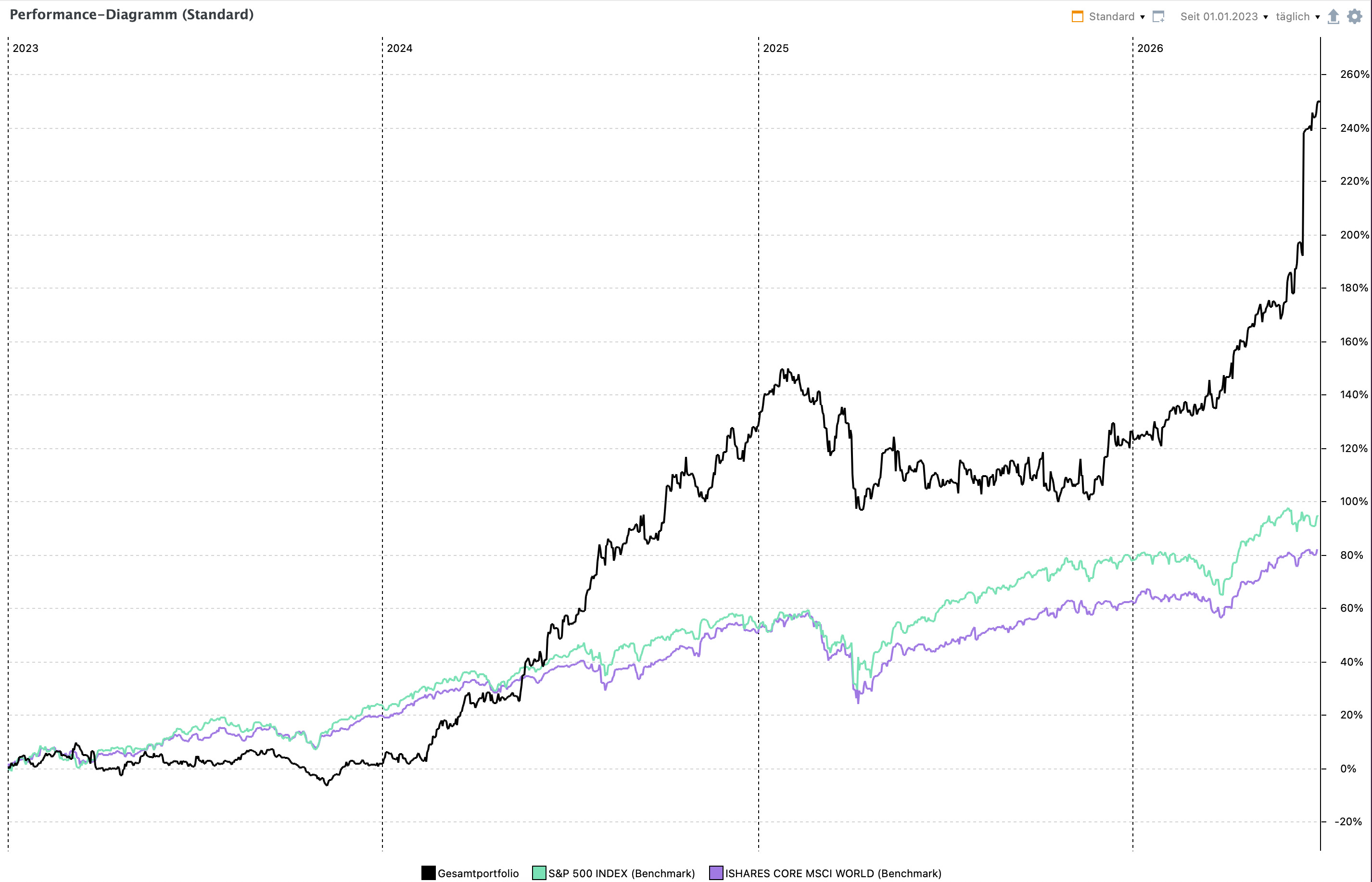

In 2024, I wrote that I don’t know if I will ever have such a great half-year again. Today I can conclude that I indeed had almost an identical half-year again.

YTD return is 55%. This brings my return since 1/1/2023 to 251%, equalling a 43.21% CAGR.

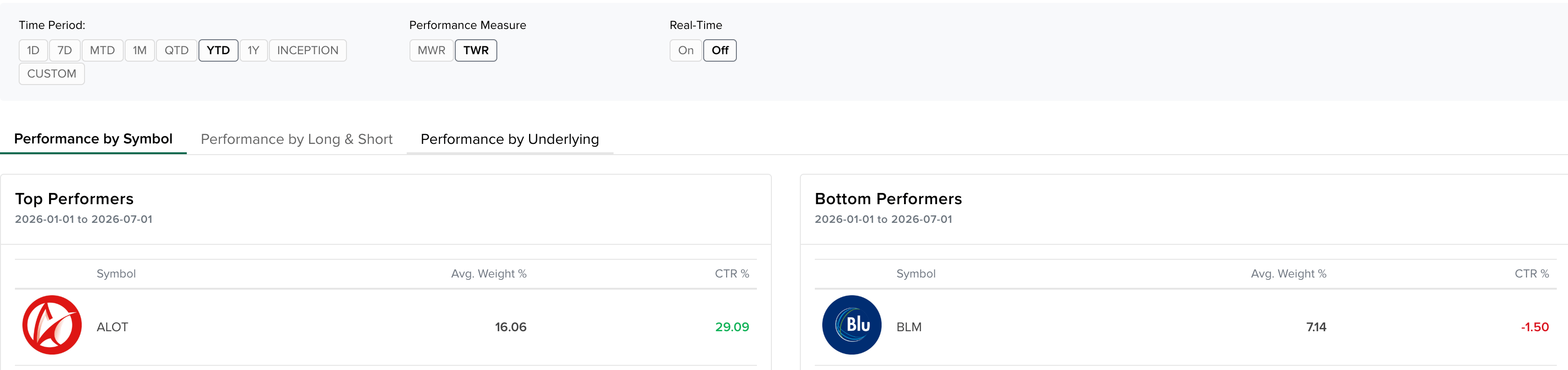

I want to emphasise that this H1 return includes a lot of luck in terms of timing. AstroNova (ALOT) was my biggest position and was just acquired for $29 per share. I wrote it up and bought shares at the beginning of the year at $9ish. While a potential segment sale was part of the bull case, a complete sale for $29 exceeded my expectations, and especially it came much, much earlier than I had hoped. Therefore it was luck that it still fell into this quarter. It could have very well fallen into 2027.

Regardless, it perfectly shows that you need one good idea per year, if it’s sized big enough in order to beat the market. If you are able to keep losses below any meaningful amount. So beating the market is simple, actually. Not easy but the formula is simple: 1-2 winners per year that are sized at 10%+ of the book and no loser that drags your portfolio down more than 2%. Then, by definition, you would come out somewhere between 30-100%. Of course achieving that is NOT easy.

What I want to say is that before this year, I barely spent time thinking as a portfolio manager, but was just focused on finding individual stocks. Of course you need both, but I’d argue especially in today’s world finding a stock that will double in the next 12-18 months is not the bottleneck. The bottleneck is to benefit from that AND even more importantly not to lose the gains with other names.

I have a Google Sheet which I use to track my trades. I have been using it the whole year. It only takes the trades I have done in a certain timeframe and compares that with the current share price. It includes all trades from this year.

Apart from buying AstroNova (ALOT) and Frontera (FEC.TO), the third most value-additive trade was to sell Sanuwave in January.

This goes back to my earlier saying. If I had done all the same on the research side, but had not sold Sanuwave, my results would be 6%+ lower.

To put this into perspective, in order to make 6% with a name, a 6%-sized position would need to double.

Learnings

I have already touched on it in the opening paragraph, as well as on this tweet:

In 2024, I had a good year as an analyst that almost accidentally also turned into a good year for the portfolio. This year, it feels much more that I have a good year as a portfolio manager. Regardless, I want to give you one learning on the analyst-side as well.

If I go through my big winners, which have been in descending order: ALOT, DBO.TO, KLNG, FEC.TO and CPH.TO, I would say that four out of those five have some kind of (yes I am going to use the word) moat…

Now let me preface this actually.

The best advice I have heard was “you always have to adjust your own tendencies” — it’s like if you’re bowling and you have a tendency to throw the ball to the left, the best advice for you in that situation is to aim to the right, in order to reach the middle.

Aiming to the right, however, is NOT the universal best advice. Some people need to aim to the left, actually.

Same in investing. I would argue that if you come out fresh out of “I just watched 100h of Buffett” school, your bias is certainly not that you need to look for better businesses, or moats.

However, for me personally, as someone who leans heavily into inflection investing/value with a catalyst, it’s a useful reminder to actively lean more into businesses with some kind of operational advantage/protection against competition.

We can also flip that: the two stocks I have lost the most money on were Finseta and IVFH, both of which had deteriorating/worsening competitive positioning.

Finseta operates in a highly competitive environment (currency exchange), and IVFH’s competitive advantage got slashed once US Foods opened up its marketplace.

So note to self: Stay away from highly competitive industries and worsening competitive positions. Focus on businesses that have some kind of advantage. You’ll get the rest (valuation + catalyst) likely right anyway, but the upside, as well as the downside, is just more attractive.