Q1 2026 Portfolio Update: Reflections on +9.1%

A good start to the year weaker market envirement

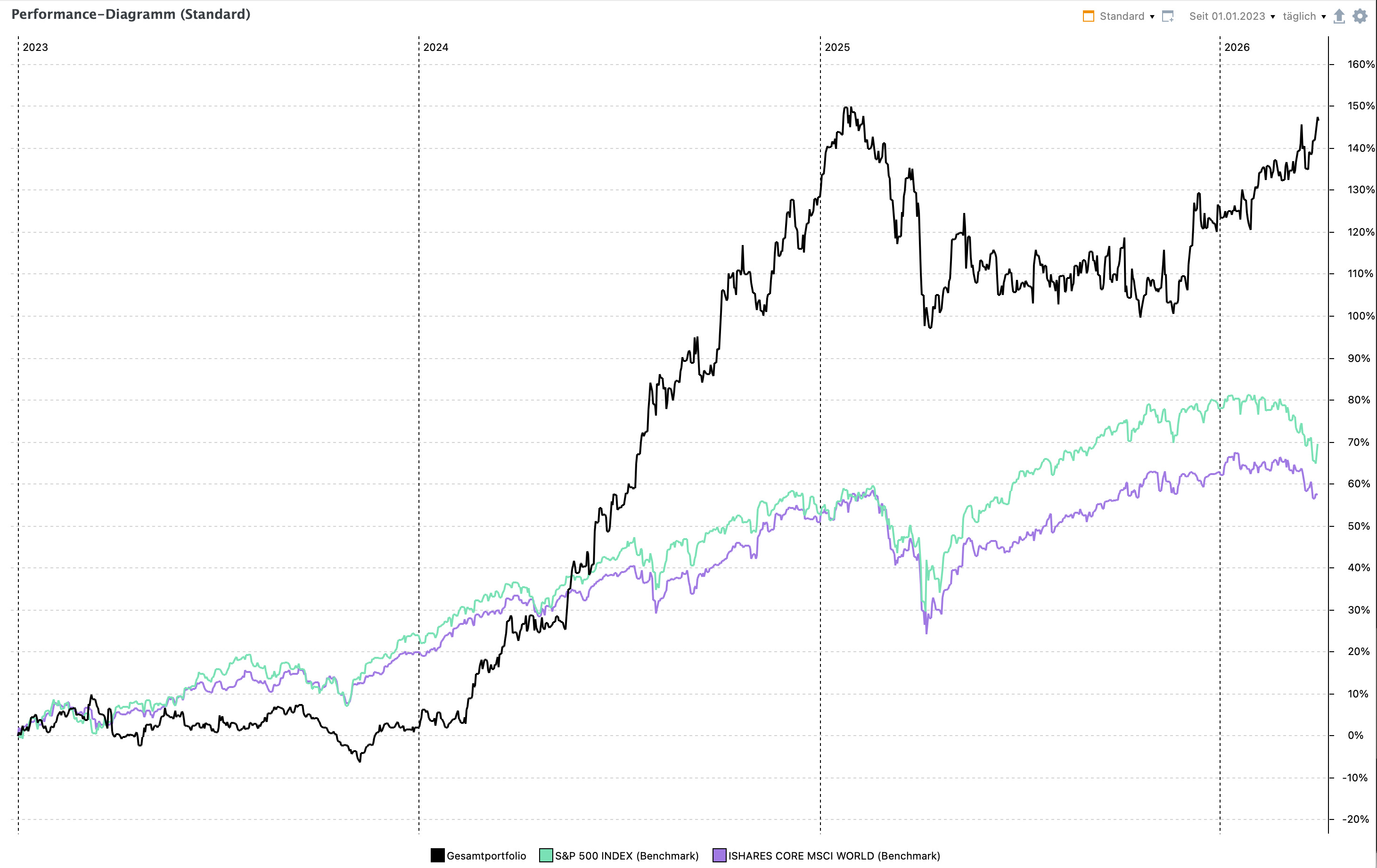

I am very pleased with my performance of the first quarter in 2026 which ended at 9.1%, and therefore compared favorably to the S&P 500, that returned -4.63%, as well as the MSCI World which returned -3.1%.

This brings my overall return, since Jan 1 2023, to 147%, which equals a CAGR of 32.1%. Compared to the S&P 500 of 70% (17.7% CAGR), and MSCI World of 57.80% (15.1% CAGR).

Mental flexibility

This outperformance was only possible by not putting myself into a box, but rather by following my hunches and — most importantly — my curiosity.

I think no one, myself included, would have expected that in Q1 2026 I would buy mainly Latin American oil companies. However, that is exactly what I did, and what led to the outperformance in Q1.

I believe putting yourself into any kind of box is a fool’s game. The only box I would put myself into is the one I think will beat the market. That can be Tech, Quality, or as it was in Q1, Oil. I don’t care if it’s in the US, Europe, Asia or Latin America. As long as the set-up is attractive and I think I have an edge, I’d be willing to go there.

Equally, I couldn’t care less about absolutes, only relatives. I don’t care if a company, country or sector is good in absolute terms. What I care about is whether it will be better than its current perception. You rarely make money on the best company if everyone knows it’s the best company — and it is priced accordingly. On the flip side, you can buy the worst company if it’s priced for bankruptcy but will actually survive. Obviously the best set-ups are somewhere in the middle, and have the greatest discrepancy between the current state and the potential future. Importantly, this change in perception can happen on multiple levels.

American stocks as a whole could experience a downgrade in investor‘s perception, while Latin American stocks could experience an upgrade. It does not matter that the US is still the richest nation and cares most about the stock market. What matters is the trajectory, compared to the current status quo. The same can happen for an industry as well as for a specific company.

Most bottom-up investors may not credit much of their returns to the first two levels, only to the last one. I believe that is only partly right. The years from 2020 to 2026 have pretty clearly showed the difference, in my opinion. Right after Covid, you had a stock market of two stocks: Covid winners and Covid losers. In 2022 — a year that 2026 is seemingly echoing — everything that benefited from inflation rose, while everything sensitive to higher rates plummeted. The years of 2023–24 were driven by American exceptionalism, fueled by the Mag 7 and a strong dollar, making everything ex-USA look weak. While 2025 looked good on paper for US stocks, it lagged most other country returns, especially measured in EUR. For European investors trading their stronger Euro into a weaker dollar to buy shares, the S&P barely did better than flat.

Anyway, it’s not about trying to predict the macro. But I think everyone who sees themselves as a bottom-up guy should acknowledge that their companies do not exist in a vacuum, but in a market driven by the perception of its participants. And that perception is what drives share prices in the short-to-medium term.

For me personally, a thesis rarely has a time frame longer than 12–24 months. I am happy to hold longer if the company continues to execute and the share price still remains attractive from a valuation perspective. However, to be frank, the IRR for most stocks decreases materially after the first 18 months of ownership, if you did time it right.

A perfect example is Cipher Pharmaceuticals (CPH.TO). I still own shares of Cipher, now for almost three years. After an unexciting 2025, also fueled by some fears around measures taken by the Trump administration around lower drug prices, shares are now positioned again for a strong 2026. Something I had already shared with my paid subscribers at the end of last year.

Operationally, Cipher has done a tremendous job all along, and yes it is more tax efficient to hold shares the whole time, but it is equally true that shares did not move for almost two years. Additionally, this is actually already the best case scenario: a micro-cap that holds its level after a run-up. Way more likely is that either the multiple gets so far ahead of the business that a bigger pullback becomes probable, or the company runs into operational problems. After all, growing a company is hard. Very hard.

All that is to say that in my opinion the stock market is about a change in perception, and that selling is equally — if not more — important than buying.

I believe a common “lazy man’s” excuse is that it is only a short-term issue and you should wait one more quarter. I think that is a very thin line, and it is actually very difficult to tell whether a problem or a trend reversal is really short-term, or how long it will last. In my experience, I have barely made money being contrarian. The easy money is buying Cipher at CA$3, when there are no expectations and you spot a new trend early. No contrarianism, no trying to catch a falling knife, just being early in an emerging uptrend.