Special Situation: A Spin-Off the Market Isn’t Pricing In (Frontera Energy, FEC:TO)

Great asset hidden in a messy structure. 90–180% SOTP upside (conservative case)

Note: I published this write-up at the end of January 2026 exclusively for paid subscribers, before the company announced the sale of its E&P segment. You can find an update here.

If you like special situations, deep value, and roadkill, here’s something for you. If you’re looking for a compounder, skip this.

This is priced for disappointment (jurisdiction + commodity skepticism) — which is exactly why the setup is interesting.

The Set-Up: A conglomerate is simplifying. It’s preparing to spin off its infrastructure business.

Even under conservative assumptions, today’s valuation appears to assign little-to-no value to the upcoming spin.

Conservative sum-of-the-parts suggests ~90–180% upside.

Two potential kickers would increase the upside further: a strategic transaction and a sentiment/regulatory shift.

Frontera Energy

Ticker: FEC:TO / FECCF

Market Cap (in US$): $316M

Enterprise Value: $689M

Price: $4.56 / CA$6.36

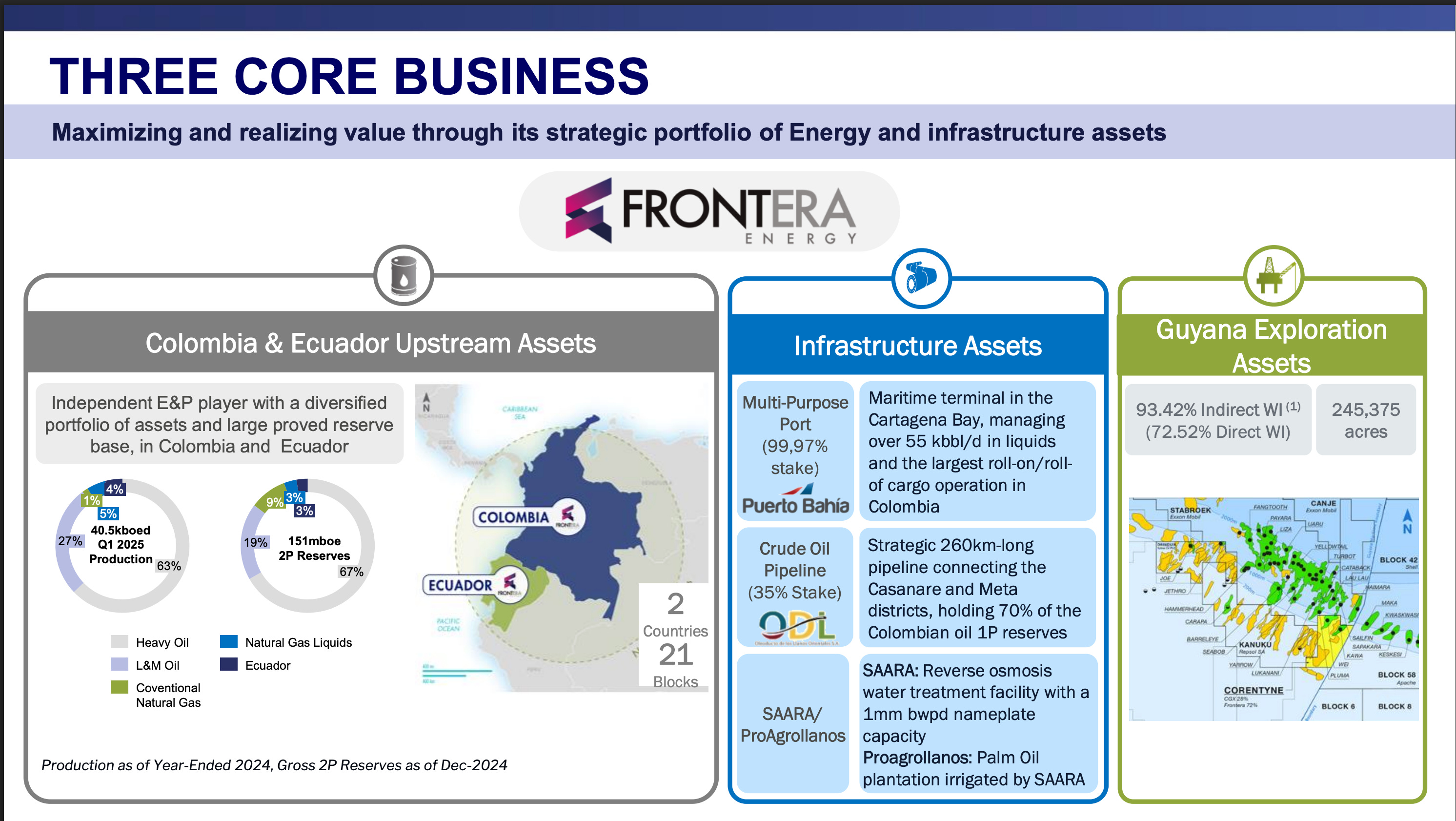

(all numbers in USD) Frontera Energy (FEC.TO/ FECCF) is a conglomerate of its infrastructure assets, which include a 35% stake in the ODL pipeline and a 99.97% stake in the Bahia Port in Cartagena, Colombia. The second part of the business consists of their onshore E&P operations in Colombia. The company announced in November last year that it would aim to spin off its infrastructure business. If the spin-off takes place, the company would finally extract the value of its highest quality asset.

Frontera Energy is perhaps the cheapest E&P company, and there are reasons for that. In 2016, the company came out of a debt restructuring process with The Catalyst Group as its majority shareholder. The Catalyst Group is a distressed debt fund with a bad reputation. There are multiple litigations against them. However, I believe it’s the first time we are aligned with them. Back in 2015, the Catalyst Group just raised money for their latest fund, Fund V. Usually these distressed debt funds have a lifespan of ten years before they aim to return the assets to their shareholders. More than ten years have passed now since the inception of their fund. I think they’re trying to cash out the assets where they can. Frontera being one of them.

The Assets

The company is best valued using a sum-of-the-parts method. And yes, most sum-of-the-parts theses never work, but with the upcoming spin-off and the steep discount, I believe the odds are stacked in our favor.

It was already communicated how the set-up will look like post spin-off.

The Infrastructure Business

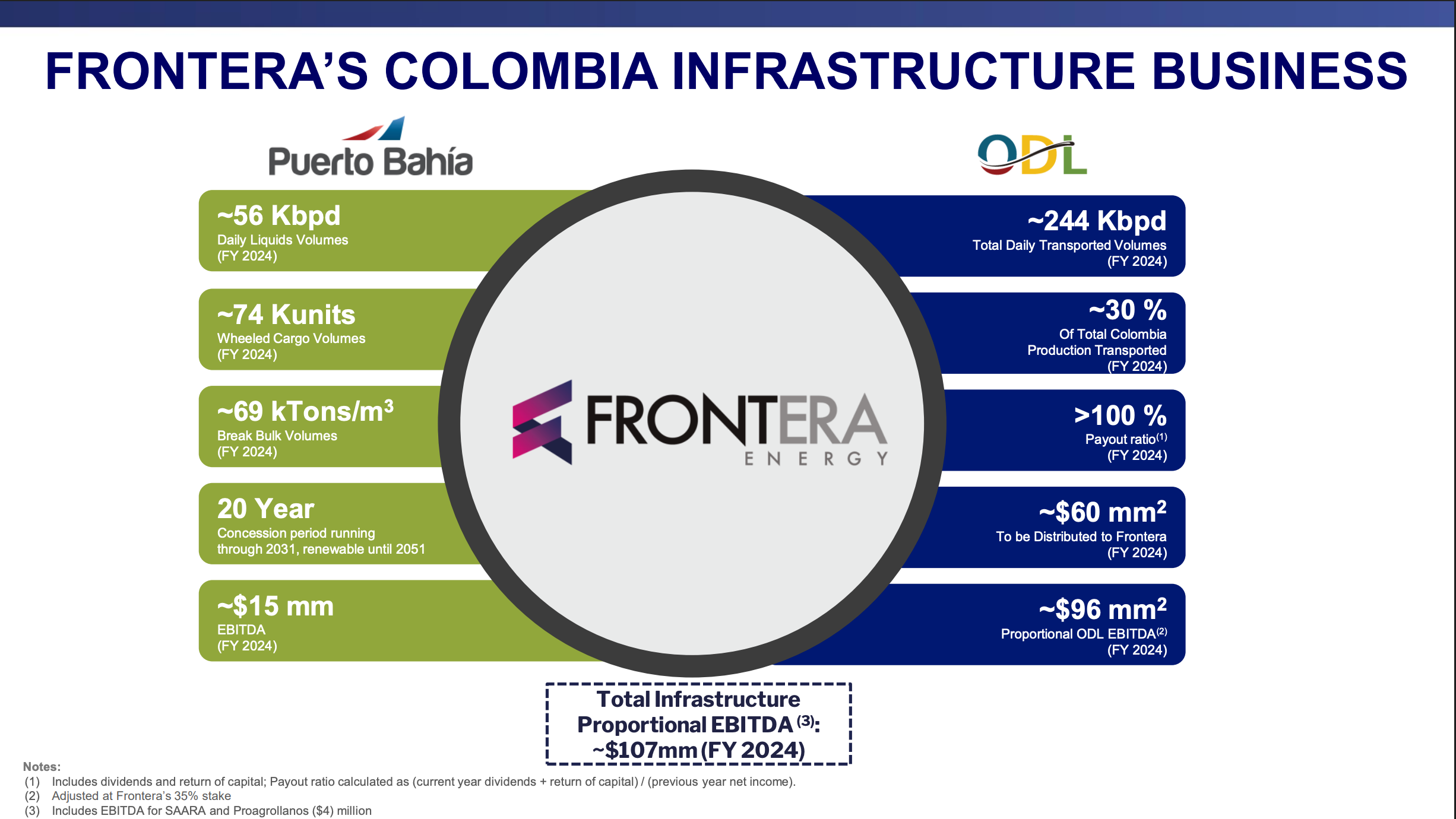

The infrastructure business consists of their 35% stake in the ODL pipeline, the port in Cartagena, and a water treatment facility, which is negligible.

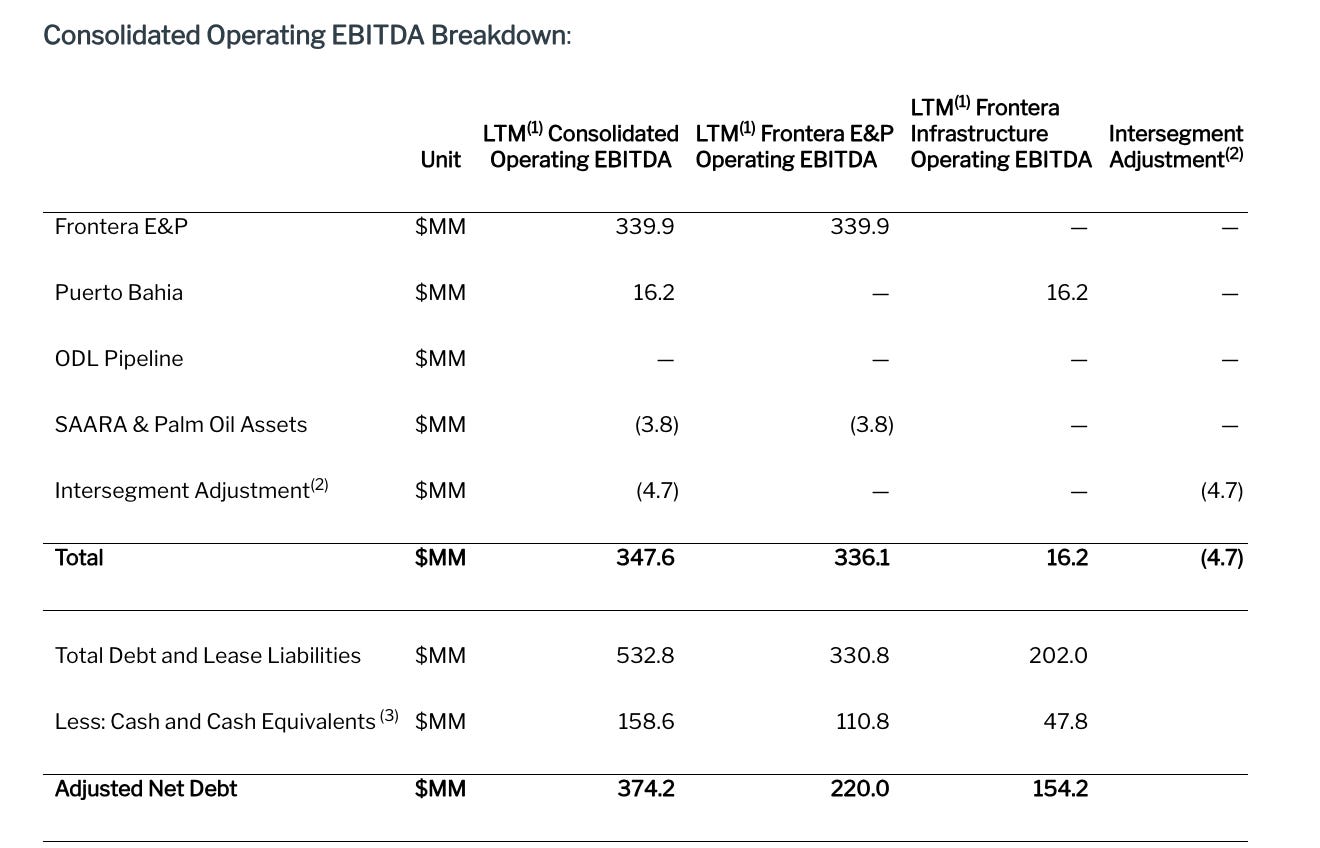

The ODL pipeline pays them an annual dividend depending on the oil flowing through the pipeline. In the last few years, it averaged roughly $60M in dividends. They have a cash-sweep agreement in place with Macquarie that these dividends will flow into the repayment of their $202M loan with them, including interest payments at 13%.

The wells from which the oil is flowing are Caño Sur, Rubiales, and Jagüey/Palmeras Stations. Rubiales is already at a mature state, while Caño Sur is expected to offset the decline of Rubiales going forward.

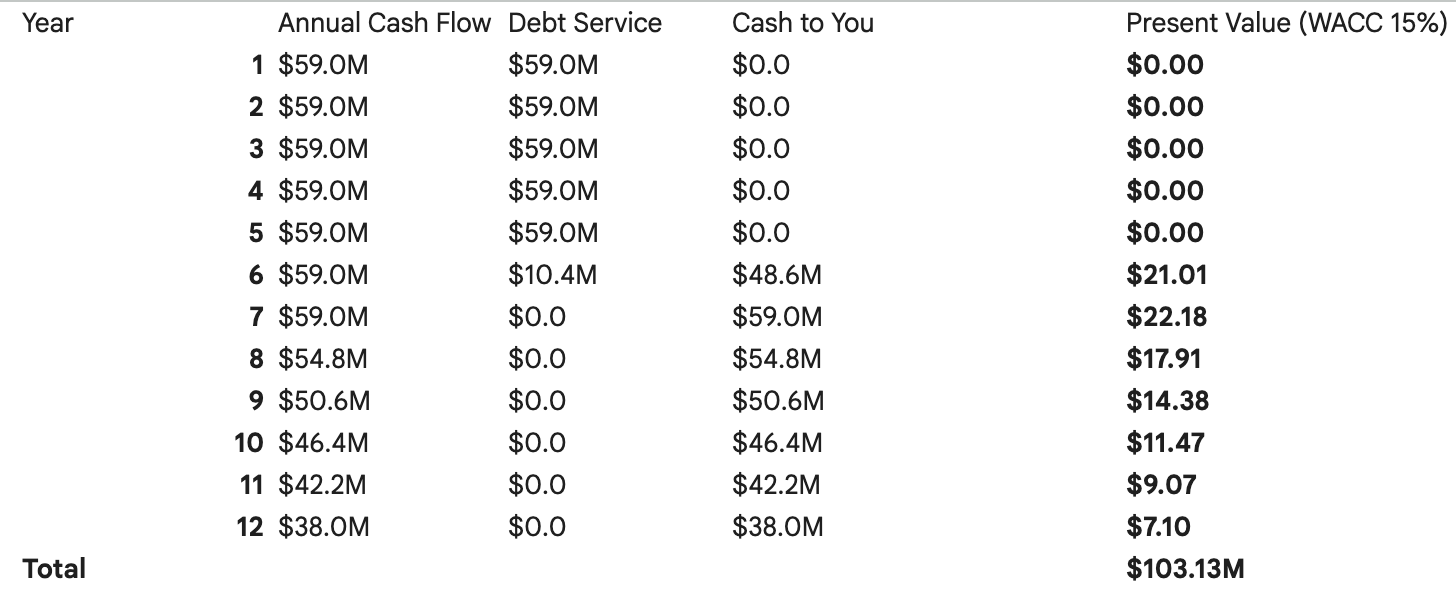

The pipeline can be valued as a constant, secure stream of cash flows. Given the fact that it’s Colombia and the reserve lives are not that long, I would assume a potential buyer would command a yield of 15%.

That would imply a valuation of $58M × 6.6 = $382M. Minus $202M debt = $180M equity value.

If you assume dividends were to shrink after year 7 to, say, eventually $38M in year 12, the present equity value would equal roughly $103M.

Valuation range ODL pipeline: $103-180M

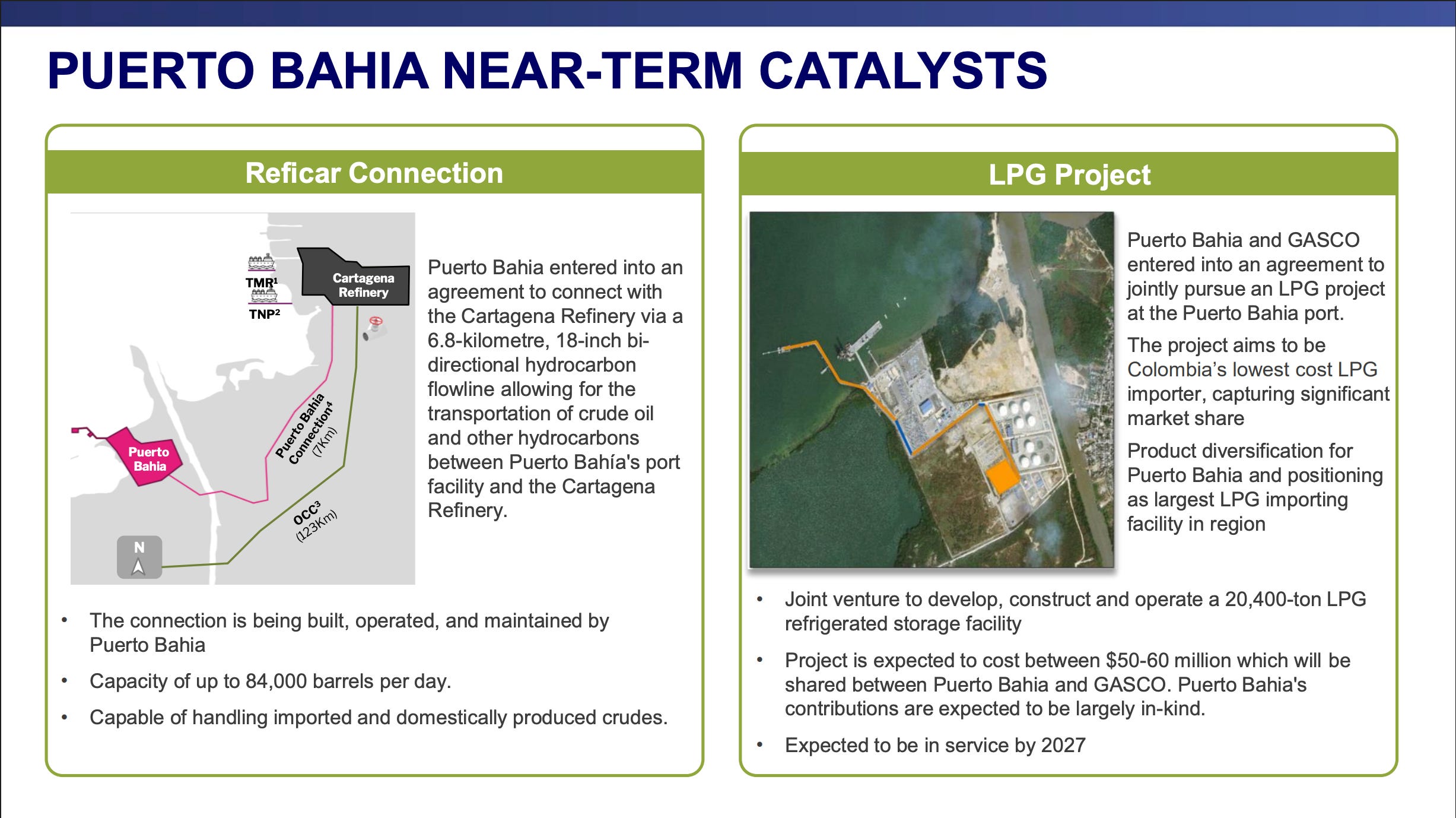

The Port

I think the port is the most exciting (or boring?) asset here. The Bahia port is one of the biggest ports in Colombia. The income streams for Frontera are roll-on/roll-off (general cargo) and oil storage. LTM EBITDA sits at $16M.

As of right now, they have two interesting projects going on. First is the Reficar connection with Ecopetrol. The connection just went live in the last quarter, and it will stabilize cash flow much more than the general renting out of liquid oil tanks, where they just lost a client. It should also increase their EBITDA from Q4 onwards, but I’m not ascribing much value to it.

The second project is their LPG terminal. It’s a gas terminal to make the import of natural gas into Colombia easier. As you may remember from Maurel et Prom, Colombia has a gas shortage and needs to import natural gas. The terminal is one of the solutions for that. The company expects that the new terminal could add another $10-15M in EBITDA once it’s running at full capacity. The terminal is expected to go live in 1H 2026. Meaning, the terminal and Reficar alone could double the EBITDA of the port from $16M to $30M within the next 2-3 years.

General cargo is also interesting. On the import side, Colombia‘s second most valued imports are cars. The peso has been pretty strong in the last two years compared to the dollar. Furthermore, more and more Colombians are able to afford a car—the rise of something like a middle class, or at least the poor getting richer (in absolute terms), is something we can see all across the region. Both the strong peso and the rise of the middle class bode well for an increase in car imports. Car imports have been on rise lately.

On the export side, livestock has been a growth driver for the port.

”For the three and nine months ended September 30, 2025, Puerto Bahia’s general cargo revenues increased by 97% and 57%, respectively, mainly due to a strong performance from general cargo operations, which saw strong growth in container volumes, that surpassed 3,000 TEUs in September 2025 and higher volumes handled, particularly livestock during the first quarter of 2025.”

MD&A Q3 2025

And this is no coincidence but driven by supply changes within LATAM. Brazil, the biggest beef and livestock exporter in the region, is in discussions to ban the export of livestock. This has led the Middle East and China to buy more livestock from Colombia than ever before, leading to record highs in livestock exports for the region in 2024 and 2025. Colombia tried to implement a similar ban, but it didn’t go through congress and is no longer discussed.

Ports are usually valued around 10x EBITDA. Given the fact we have a sub-scale operation in Colombia, I’m using 8x EBITDA. Valued on LTM numbers, that would total $128M. Based on NTM (my estimate), it would likely be $160M ($20M × 8).

Add now the $47M in cash and we get to $175M + $207M.

Total valuation range net of debt for the infrastructure asset: $278-387M

Current market cap in USD of the entire business: $313M.

The Bad Asset

The remaining asset, which is currently valued at $0 in my opinion, is their E&P operation in Colombia. The point is not to determine whether this is a great asset or not, or if oil goes to $100/bbl. The only task at hand is to figure out if the asset is worth more than $0. If yes, we would likely make money.

As of right now, they have 36,000boe/d in Colombia. Most of it is heavy oil. The cost to produce a barrel is therefore higher than with light oil operations.

In the past, they have tried to diversify away from Colombia by exploring into Guyana. The government ended up seizing their assets. They lost +$300M. It’s still an ongoing lawsuit. I ascribe $0 value to it, but potentially they could still get some money out of it

At $65/bbl, they guide to $270M in EBITDA substracting maintance capex of $160M, you would get to $110M, substract $25M in interest and you have roughly $85M pre-tax free-cashflow. Colombia has a a tax system depending on the surplas of oil prices, meaning at $65/bbl, they would pay only $0-$5M in cash taxes.

Colombian oil producers are trading at a deep discount. Usually 2.5x EBITDA. Reason for that is lower reserve lives of 7-10 years, and it’s usually not as profitable because it’s heavy oil that is sold discounted. I also believe that multiples have stayed low since the election of Petro and his “anti-oil” stance (more on that later).

The two ways to value the company: one is by EV/EBITDA. In that case, I would assume a 2x EV/EBITDA multiple to be fair. Valuation at $65/bbl in that case: $270M EBITDA × 2 = $540M. Minus $220M net debt = $320M equity value.

A buyer, however, would likely ignore that since oil prices fluctuate and look at what they’re paying per flowing barrel. And here, the discount becomes very apparent.

They have produced 36,000 boe/d. The current EV (excl. the debt of the port) is $533M. Meaning the company is currently valued at $15k/flowing barrel. That's by far the cheapest oil producer in Colombia.

As a matter of fact, there hasn’t been any transaction I could find in the region below $25k/flowing barrel. The GTE/Petroamerica transaction in 2015 was at $28k/flowing barrel. The Oxy/Carlyle (SierraCol) at $25k/flowing barrel in 2020.

Just recently, GeoPark, a Colombian producer, rejected an offer from Parex, another Colombian producer, for $35k/flowing barrel. Granted, the oil of GeoPark is lighter and has a lower breakeven price than Frontera’s oil. (read here)

But, while the valuation of $15k/barrel did not include the net debt of the port, it still includes the calculated equity value of the infrastructure asset. Meaning the actual implied value per flowing barrel is even lower than the $15k/barrel.

Even if the company were to get acquired at what would mark most likely the cheapest deal for 38k boe/d, we would get the value of the port on top of that. Implying $300M+ upside.

At a reasonable, still low valuation of $20k/flowing barrel, that’s $760M - $220M net debt = $540M.

Valuation range for E&P: $320-540M

Total equity valuation range: $598-927M, or $8.71-13.00 USD per share. Current share price: $4.55 USD.

Potential upside: 91-185%.

Why Now?

As I alluded to before, I believe Catalyst Group is aiming for an exit. They have tried to sell the company as a conglomerate back in 2023 and did not succeed. The spin-off is very likely the first step to a sale of the infrastructure asset. I actually believe they may already have a buyer. Macquarie already owns the debt of the ODL pipeline. The cash sweep agreement means they’re already getting paid. They would naturally be the most aligned buyer if the cash sweep goes back to your own pockets. It would also fit, given the fact they just raised US$8 billion.

Other usual suspects would be infrastructure funds like Brookfield that have been investing into Colombia recently.

The Political Kicker

Talking about Colombia. I think the timing is also not a coincidence. In 2022, Colombia elected its first left-wing president in a long-time, Gustavo Petro. While he was not able to pass any meaningful laws through the constitution, the money from the outside has fled Colombia since then. The last elections in South America have all shifted to the right, from Argentina and Bolivia to Chile. More importantly, Petro’s approval ratings are extremely low. He also cannot run for president again.

As of right now, the two top candidates for the upcoming election in May are Iván Cepeda Castro and Abelardo de la Espriella.

De la Espriella is perceived to be an “ultra-right-wing” candidate who has his own business and, to quote a Colombian Reddit user, “would sell his grandma for money”—sounds like the next best friend of Trump if you ask me ;).

His opponent is likely a continuation of Petro’s “failed” policy. In the recent poll, the right-wing candidate was leading. While I don’t know if he will win, if he does, it would be a perfect catalyst for the company as well. Most likely he will stop the exploration ban, make Colombia more business-friendly, and push valuations up.

Just imagine, Colombian oil producers not trading at 2.5x EV/EBITDA but at 3.5x!!!! Now, apply $70/bbl+ prices… I’m losing the plot and start to dream.

Anyhow, there are still a series of events that have to happen to increase the upside here. While the probability of all of them happening is certainly lower than I’d like them to be, I believe there are reasons to believe they will happen, and now is the time.

How to Lose Money

If none of these events were to take place—meaning there is no spin-off, Colombia elects a left-wing government, and oil goes to $40/bbl—then the E&P might actually be worthless. Well, in an absolute worst-case scenario, they burn cash, struggle to refinance the debt in 2028, and dilute equity holders to save the company. In that case, you could assume a $0 for the E&P. I think it’s unlikely. Probably in such an event, a buyer could potentially step in. Even if they had to repay the bondholders, it could still make sense to buy the assets for cheap. As outlined above, in the case that E&P is valued at zero, the infrastructure business is likely already worth the current market cap. Furthermore, after the spin-off, there is also no need to keep holding shares in the E&P. So they just have to survive the next 6-12 months for the trade to work out.

If the spin-off doesn’t take place, they could likely lend against the debt-free port.

But if you think the company is able to refinance its $320M unsecured bonds until 2028, then you may be interested in buying the bonds. They are trading at 70 cents on the dollar, with a 7.8% coupon and expiration in 2028. I’m not a bond expert, but to me that’s a pretty attractive yield.

Conclusion

I think the company is very cheap, too cheap, even though it has a lot of hair. The spin-off should serve as a great short-term catalyst. Hard-to-measure events like the election in Colombia and the price of oil will dictate how big the potential upside can be. The price we’re paying, however, protects our downside, even if both of these events turn out negative.

For me, therefore, it’s a 5% position. I’ll track elections and the price of oil closely, and could imagine increasing the position if one or both events turn favorable in the coming months. The same goes, obviously, for any progress related to the upcoming spin-off.

If you want to receive my next idea into your inbox, become a subscriber:

Disclaimer: The content provided in this newsletter is for informational and educational purposes only and does not constitute financial, investment, legal, or tax advice. The views expressed are my own and based on my own research. I am not a financial advisor.

Disclosure: As of the time of this publication, the author holds a long position in Frontera Energy (FEC.TO / FECCF). The author may buy or sell shares at any time without notice. Do your own due diligence (DYOR) before making any investment decisions.