The Cheapest Oil Stocks in the World

And there are reasons for that.

Colombian Oil producers are still amongst the cheapest equities in the entire stock market. EV/flowing barrel is below $32,000 for all companies. EV/1P reserves are valued below $10/boe. EV/EBITDA (NTM on $60-65/bbl) is between 2.6-3.2x. On every metric, these are the cheapest oil companies I can find.

And there are reasons for that. Politically, the country has done the oil sector no favours — quite the opposite. With current policies the country will run out of oil in 7 years. However, most of these Colombian E&Ps are not pure-play Colombian businesses anymore, or at least are planning on not staying that way. Yet all of them trade much lower than their historical mean valuation (based on $60-65/bbl forecasts), and also much lower than state-owned Ecopetrol, which is already trading above its mean.

On top of that, each company has somewhat exciting developments going on that can unlock value for shareholders. A consolidation is underway, and soon we will have one clear big independent player behind Ecopetrol, producing 90,000+ boepd. Two of the players are expanding into other Latin American countries like Argentina, Ecuador, and Venezuela. All while trading below 3x EV/EBITDA. And with oil at $75/bbl or above, one of these companies would be trading at a free cash flow yield north of 50%.

That’s what I call layers of catalysts. I own two of these players.

Why now?

Investing in cyclicals is all about timing, and I believe there are potentially multiple catalysts hitting here. Some broader, others country-specific, others company-specific.

The “safe barrel” trade

With the current war in Iran, potentially 20% of global oil supply is at risk. Colombian barrels are untouched by this. The crude flows from the Llanos Basin to the Caribbean port of Coveñas via pipeline, then five days by tanker to the U.S. Gulf Coast. No Strait of Hormuz. No Suez Canal. No tanker war insurance premiums. Atlantic basin barrels, listed on Western exchanges in Toronto and London.

These companies don’t just benefit from higher oil prices. They benefit from a repricing of risk. When capital rotates out of Middle East-exposed energy assets and into “safe” producers, Latin American E&Ps are a natural destination.

Colombia obviously has its own risks. Pipeline attacks, political uncertainty, heavy crude discounts. But those risks are uncorrelated with the ones dominating headlines right now. A Hormuz crisis doesn't make Colombia worse.

The election catalyst

Colombia holds presidential elections on May 31, 2026. Petro cannot run again. Every major center and right-wing candidate is campaigning on reopening exploration and allowing fracking. Even Claudia López, the center-left former mayor of Bogotá, reversed her anti-fracking stance in 2025, calling cheap energy the best predictor of industrialization. Cepeda is the only major candidate who would maintain the moratorium. Colombia currently imports natural gas at steep premiums because domestic production cannot meet demand. Voters feel this on their utility bills. A center or right-leaning president would reprice these stocks almost overnight.

But here’s the key: the thesis does not depend on a right-wing victory. If the moratorium continues, existing operators are already positioning themselves to grow outside of Colombia. That shift would only accelerate if the current stance on fracking remains after elections.

Colombia, a brief overview

You are probably asking yourself why I am writing about Colombian oil producers. Honestly, I would not have guessed this half a year ago. But my curiosity led me there.

Despite being known for its violent past in the 80s and 90s, Colombia has improved and stabilized since then tremendously. They have one of the oldest democracies in all of Latin America. The country was usually known for its right/center-leaning politics, especially during the eight-year tenure of Alvaro Uribe, a right-wing politician, from 2002-2010. He was responsible for a pro-oil agenda. His 2003 reforms created the ANH, opened the sector to foreign investment, and triggered a production boom from ~530,000 bopd to over 800,000 bopd by the time he left office. Production continued climbing to an all-time high of ~1,008,000 bopd in 2013 under his successor Santos.

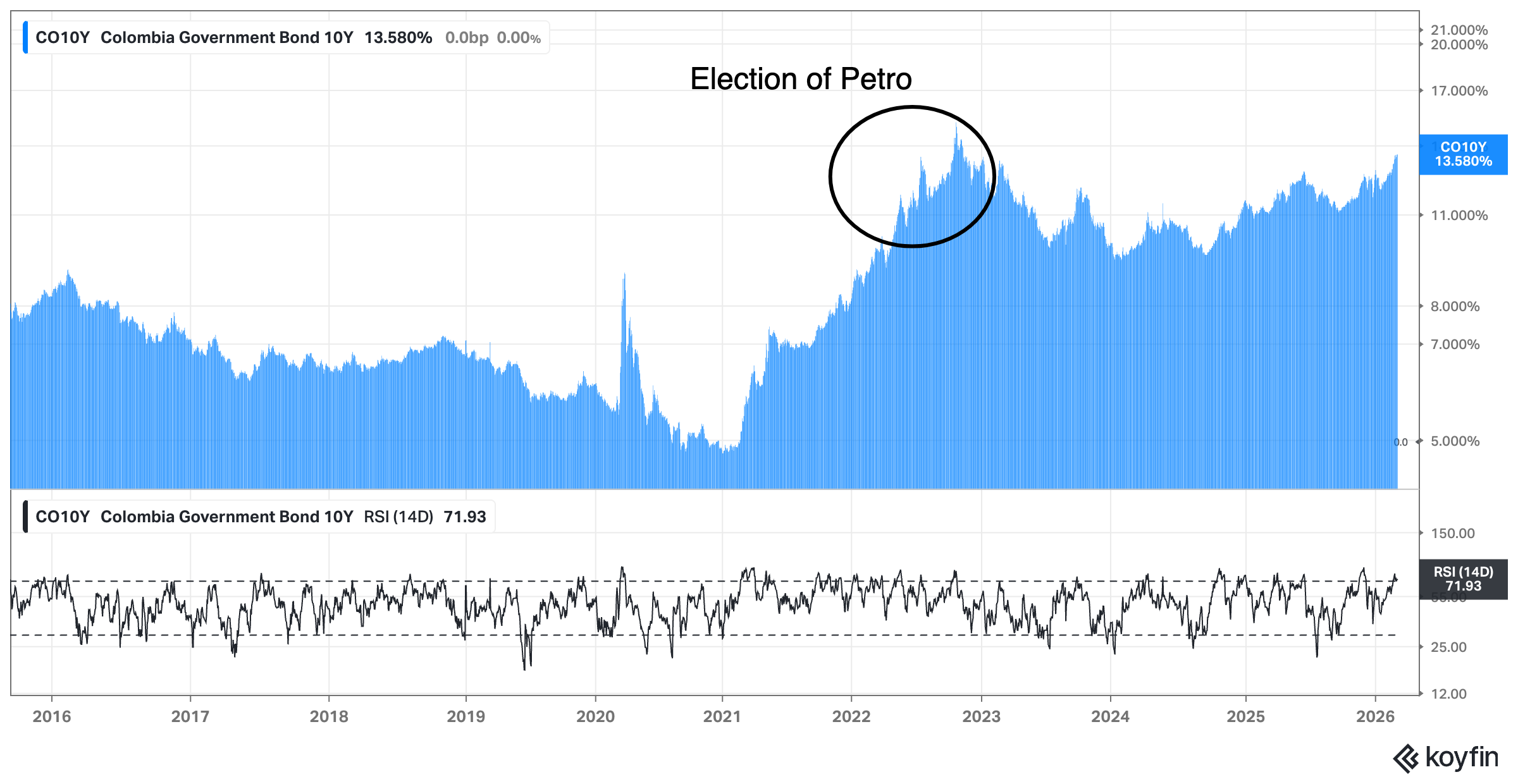

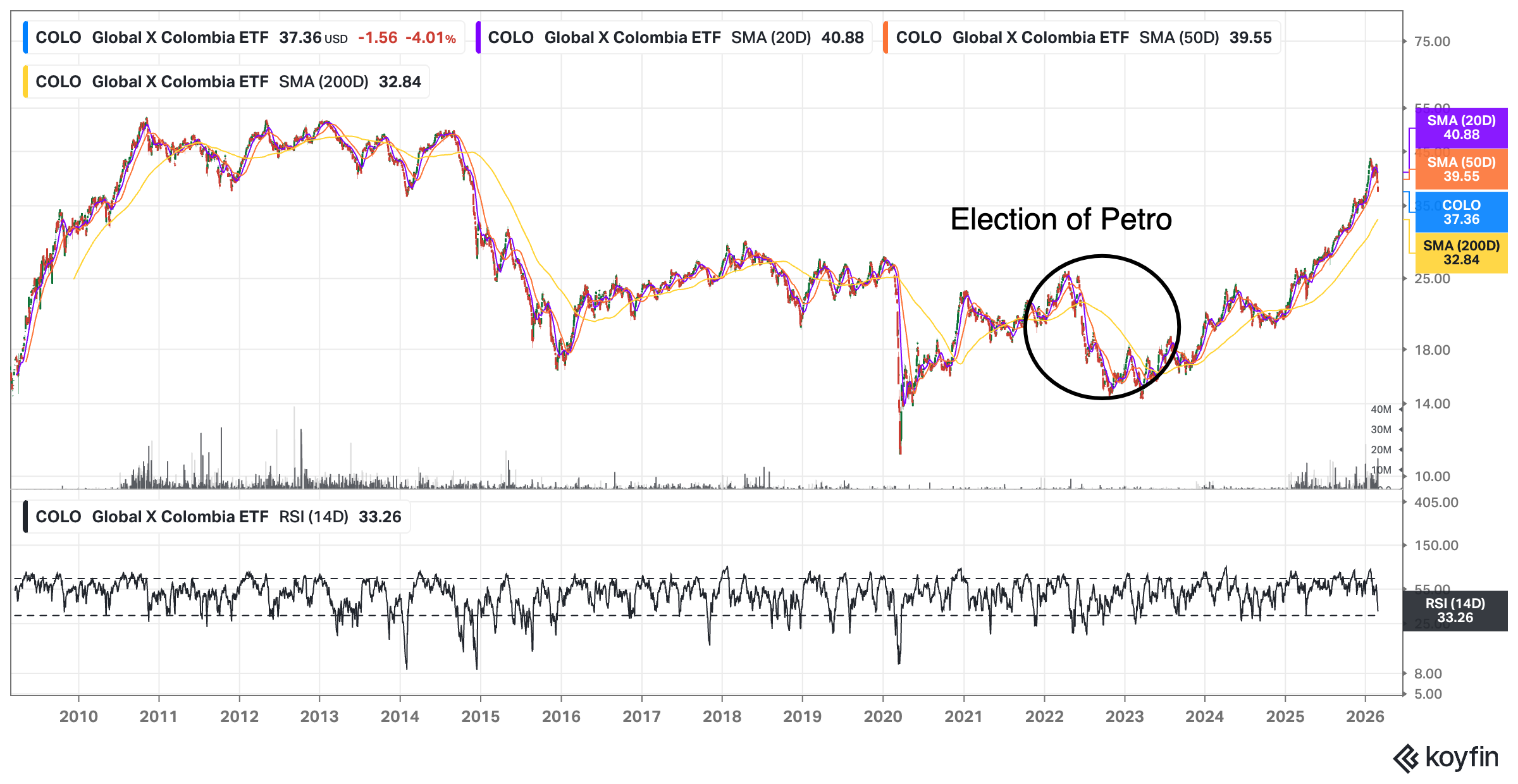

However, this changed when Gustavo Petro won the elections in 2022. The reaction from the market? The Peso crashed to COP5000/USD, and the 10-year yield climbed to a record high of 14%.

Consequently, the stock market crashed as well:

Importantly, Petro never had power over the parliament. He couldn’t do much “damage” — most of his proposals never passed congress. Recently seen by the suspension of his (ridiculous) 23% proposed hike in minimum wage. The court threw it out. A clear example that the parliamentary system in Colombia works, and that the country can actually be seen as politically stable.

The overall economic situation is not exciting. GDP grew 2.3% in Q4 2025, below forecasts, with inflation around 6%. But it’s also not horrible. Probably still good enough that common-sense policies could see a material improvement.

The upcoming elections

This weekend’s parliamentary elections gave us the first real signal. Paloma Valencia, the Centro Democrático candidate backed by former president Uribe, won the right-wing consulta with 3.2 million votes, roughly 59% of the primary vote. That’s a serious number for a primary. The right came out of March 8 looking united and energized.

The presidential field has now narrowed to roughly six candidates for the May 31 first round. Cepeda leads the polls and will carry the left. De la Espriella is the hard-right independent who has been rising fast. Valencia now enters as the official center-right coalition candidate. If she and De la Espriella consolidate, the path to a pro-oil presidency looks increasingly plausible.

In Congress, neither side won a majority. Petro’s Pacto Histórico gained 5 Senate seats, but Centro Democrático gained 4. The parliament remains fragmented, which, as we’ve seen over the past four years, actually works in investors’ favor: it means no president can do too much damage in either direction.

Importantly, they don’t need a Milei. The country, albeit with 6% inflation, is not in ruins. A lift in regulations would be bullish for regional perceptions.

That being said, let’s dig into each of the smaller companies. I will not cover Ecopetrol, it’s already well covered, state-owned, and much more expensive. There are only four independent players. Soon, only three. I own two of the three companies I'm covering here, plus Frontera Energy which I've written about before.