Updates on IVFH, SGRP, CSFS.L &0869.HK

Commentary on the earnings of the profiled companies

There will probably be future updates that are difficult to write. This update is not one of those. All the profiled companies reported good earnings and optimistic commentary regarding their future. Let’s dive right in.

Q1 2024: Innovation Food Holdings (Ticker: IVFH)

Innovation Food Holdings reported their Q1 numbers on Tuesday and held their earnings call later that day.

The results are still messy, but we are starting to see progress. For the first time since the technology change at their largest customer, the foodservice business grew again, although only 1.6%, this is a great achievement.

Gross margin continues to increase as they continue to wind down their e-commerce business and focus on their foodservice arm. In addition, for the first time in five years, they reported a profit in Q1. adj. EBITDA came in at around 400k, so with the e-commerce business still a drag on their profitability and Q1 being the slowest quarter, this is already a great accomplishment.

The e-commerce business and their warehouse both have potential buyers interested in buying them. This would give the company a nice infusion of cash and, as Bill said, is one of the requirements to lay the foundation for growth1.

A glance into the future

Once the e-commerce business is completely shut down (or sold), what will be left is their drop-shipping business serving food distributors and their traditional food distribution business serving restaurants in the Chicago area.

The drop-shipping business is as good as it gets. Not only do they have a unique offering, there is no comparable business, but it is also a very asset-light business model that enjoys high margins and does not require capital to scale.

As a result, management is focused on growing this part of the business, which was neglected by the old management and mainly served one customer, US Foods. Already this year, Innovation Food Holdings has added two new customers to its drop-shipping business2. If you read their press releases, they say that it takes several weeks or months to integrate their platform into the client's business. That gives you a sense of how deeply integrated they are into their customer's business. Once they are in, they are in.

For the traditional business, the growth strategy would involve a typical M&A strategy, Bill has already briefly explained what his goals would be in that regard. Depending on how well the drop-shipping business can be scaled, the future company will probably be a combination of both businesses, but 10 times the current size. Innovation Food remains my best idea and biggest position.

Q1 2024: Spar Group (Ticker: SGRP)

Spar Group recently sold its joint venture structure. The thesis is that after this sale, the company will not only have a simpler financial structure, but should also return money to shareholders and benefit from higher margins and industry tailwinds. After this quarter, we can check all those boxes.

Operating income of $9.6 million included $7.2 million from the sale of their South African JV. After the sale of the Brazilian JV, most of their sales will be generated in the US and Canada, which grew 22% in Q1 as the remodeling business rebounded and contributed to this growth. Canada in particular is impressive with 70% growth, albeit from a small revenue base.

The gross margin was compressed to 18.3% in the quarter, compared to 22.3% in the same quarter last year. The South African business was the reason for this, and management said it should quickly return to historical numbers. In general, the South African business seemed to be a drag on the margin, as was the sold Brazilian venture, which was confirmed to have a lower margin than the US and Canadian operations3.

The biggest risk remains that they make a value-destroying acquisition. Management has done a good job so far in my opinion by selling the joint ventures, increasing gross margins and buying back shares from the old founder, in addition the board has a background in M&A which can also be a positive. Overall, I remain excited about the next few quarters. The thesis is intact.

2023 Annual Results: Cornerstone FS (Ticker: CSFS.L)

Cornerstone reported its 2023 numbers. Previously, the pro forma numbers had been announced, so the reported numbers were no big surprise.

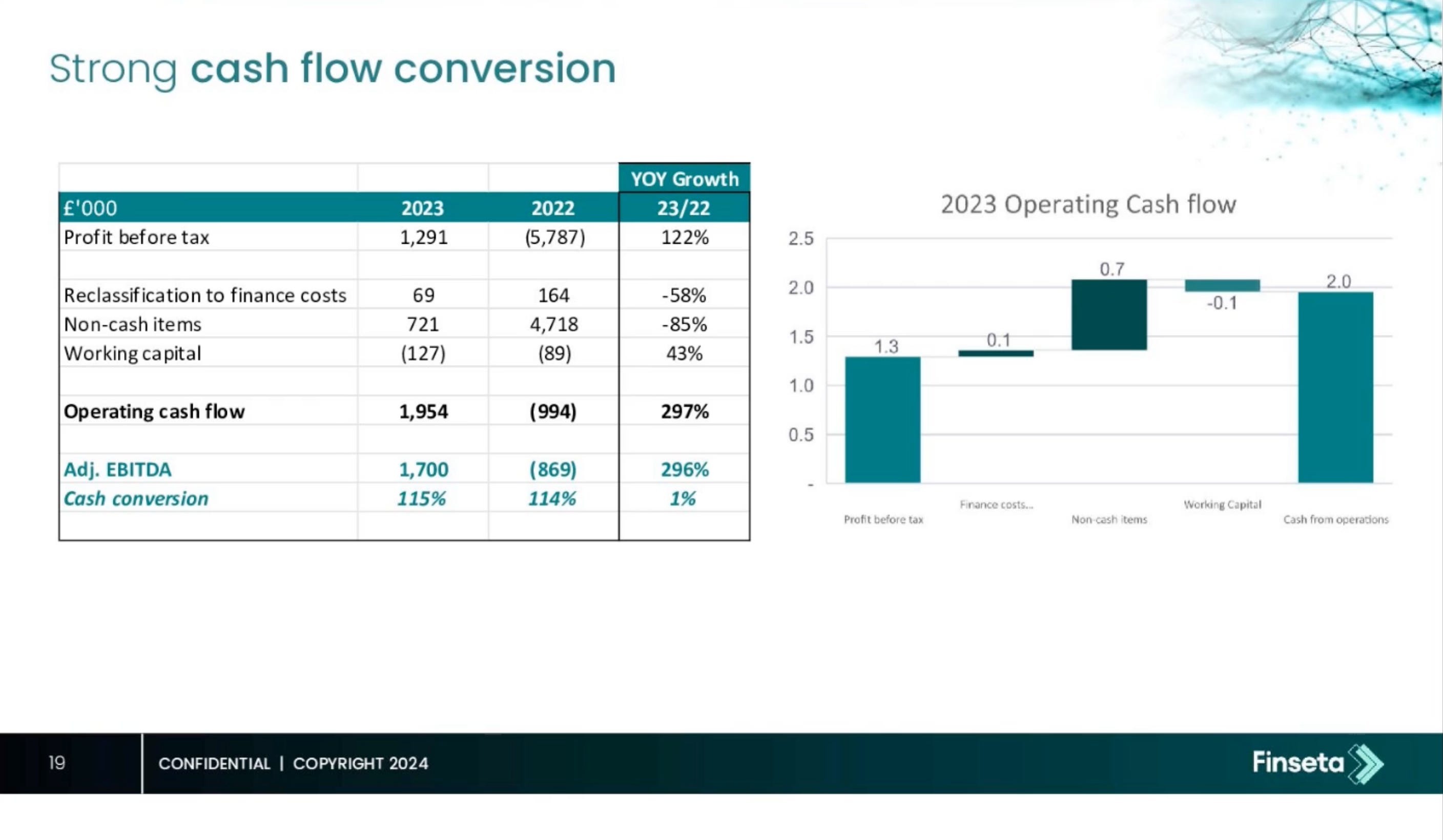

Nonetheless, the numbers are just impressive, they grew revenue by 100% and £1.7m in adj. EBITDA. The cash conversion of this business is impressive as well.

Manamgent said that the transition from white label to direct clients (HNW) is now complete. They have cut all white label clients, which will be a small drag on their revenues in H1 compared to last year and H2 of 2023.

Also, they won't continue to grow revenues by 100%, but rather by 20-30%. By my calculation, 25% revenue growth should lead to about £2.5m of adj. EBITDA, resulting in a valuation of less than 10x EV/EBITDA. The EBITDA to operating cash flow conversion is shown above, and the capex is neglectable.

The thesis remains intact, and I am excited about their H1 results. A new agreement with Mastercard, additional salespeople and a new license in Canada should contribute to their growth.

Positive profit alert: Playmates Toys (Ticker: 0869.HK)

Playmates issued another positive profit alert, this time for their Q1 numbers. The launch of King x Godzilla went very well. Toy sales and box office numbers are excellent. Resulting in a great Q1. Most likely, the first half of 2024 will see good numbers and another dividend.

In summary, every thesis so far remains intact. Some ideas are higher quality than others, but all have a place in my portfolio at this time. I look forward to the next quarterly update on these companies.

Disclaimer: This is not investment advice and meant for entertainment purposes only, I hold positions in the discussed companies and therefore may be biased in my opinion.

Earnings Call transcript: https://www.ivfh.com/static-files/26bf46dc-01db-4cf2-9b9f-feeaca62bdd2