Overlooked MicroCap: Parks! America ($PRKA)

Software-like margins protected by a local moat

Edit: This is a closed idea, I know longer own shares in Parks! America

Overview:

Parks! America (PRKA) owns and operates three regional animal safari parks, one in Pine Mountain, Georgia, another in Strafford, Missouri; and another in Bryan, Texas.

A regional animal safari park is basically a drive-through zoo. Meaning a customer either drives through the park with his own car or rents a car at the park.

In an animal safari park the customer enjoys several animals such as giraffes, zebras, deer and many more and can feed them from their car.

If you want to get an impression, you can watch this video on YouTube:

A ticket costs between 18-26 Dollar and each park has great reviews on Google. 4,5 stars for the parks in Georgia and Missouri and 4,3 for the new Park in Texas, which has been acquired for 7.1 million Dollar in 2020.

I believe the business model is attractive for several reasons:

It is very capital-light.

Once a park is acquired, it requires very little capital to grow and maintain. The animals reproduce themselves, the customer pays for the food because they feed the animals, therefore they generate gross margins of around 89%.Natural Moat through location

Even though they compete against other forms of entertainment, no one will place a similar park next to them. Hence, the business should be protected from competition.They have pricing power

In the entertainment sector, a company sells an adventure. No family wouldn‘t buy the ticket, if it would be 2-3 $ more expensive.Recurring Revenue

If you read their reviews, a lot of people are saying they will come back soon. This is especially important after their huge increase in demand during covid, which brought a lot of new visitors, so it is reasonable to assume some of them will come back even after Covid.It is very durable business

Fascination with animals has been around since people can think basically, also zoos and parks have been around for a very long time.

Management:

Dale Van Voorhis has been the CEO since 2011, he is already 80 years old and has over 55 years in the entertainment and amusement industry. He takes home a modest salary of $125.000 (including Bonus) and owns 21,3 % of all shares outstanding.

Besides the CEO, Charles Kohnen, a director, owns 29% of all shares outstanding, and has purchased more shares on the open market this year. Overall about 52% of all shares are held by insiders.

The management never paid a dividend and emphasized they have no intention to do so in the future. Instead, they want to focus on growing the business and acquire more theme parks. Nonetheless, they waited 8 years to make the first acquisition by acquiring the park in Texas.

Fortunately, they were able to acquire the park without diluting shareholders.

“We believe acquisitions, if any, should not unnecessarily encumber the Company with additional debt that cannot be justified by current operations. (...) By using a combination of equity, debt and other financing options, we intend to carefully monitor stockholder value in conjunction with the pursuit of growth.” - 10K

Recently they added two new members to the board.

Lisa Brady aged 35 - making her the youngest board member - who “brings more than a decade of experience in the entertainment, leisure, and hospitality industry with executive-level experience in strategic planning, mergers and acquisitions, investor relations, financial modeling, and real estate development.” (Annual Report, 2021)

The second member is Rick Ruffolo who has a background in consumer goods marketing.

In addition to that, they hired a consulting firm in 2021:

“We engaged an experienced amusement industry consulting firm to assist us in developing a master plan for our Georgia Park. Our 2022 fiscal year capital plan includes the first major project within that master plan, an impressive giraffe exhibit. This exhibit will be a new showcase for our Georgia Park, allowing our guests to encounter our giraffes regardless of weather conditions or outside temperatures. In aggregate, our 2022 fiscal year capital investment plan involves nearly $3.0 million of improvements across all three of our parks. This significant increase in capital investment spending will be fully funded from our existing cash, and demonstrates our commitment to building for long-term, sustainable growth.”- 10k Annual report 2021

The new board members, the engagement of the consulting and Master Plan above clearly shows management wants to grow the business. However this will come at the expanse of current free Cash Flow, as they stated they will invest around 3 million in 2022.

All in all I believe that management is very well experienced and knowledgeable in the industry and are determined to grow the business and allocate the capital reasonably to increase long term shareholder value.

Financials:

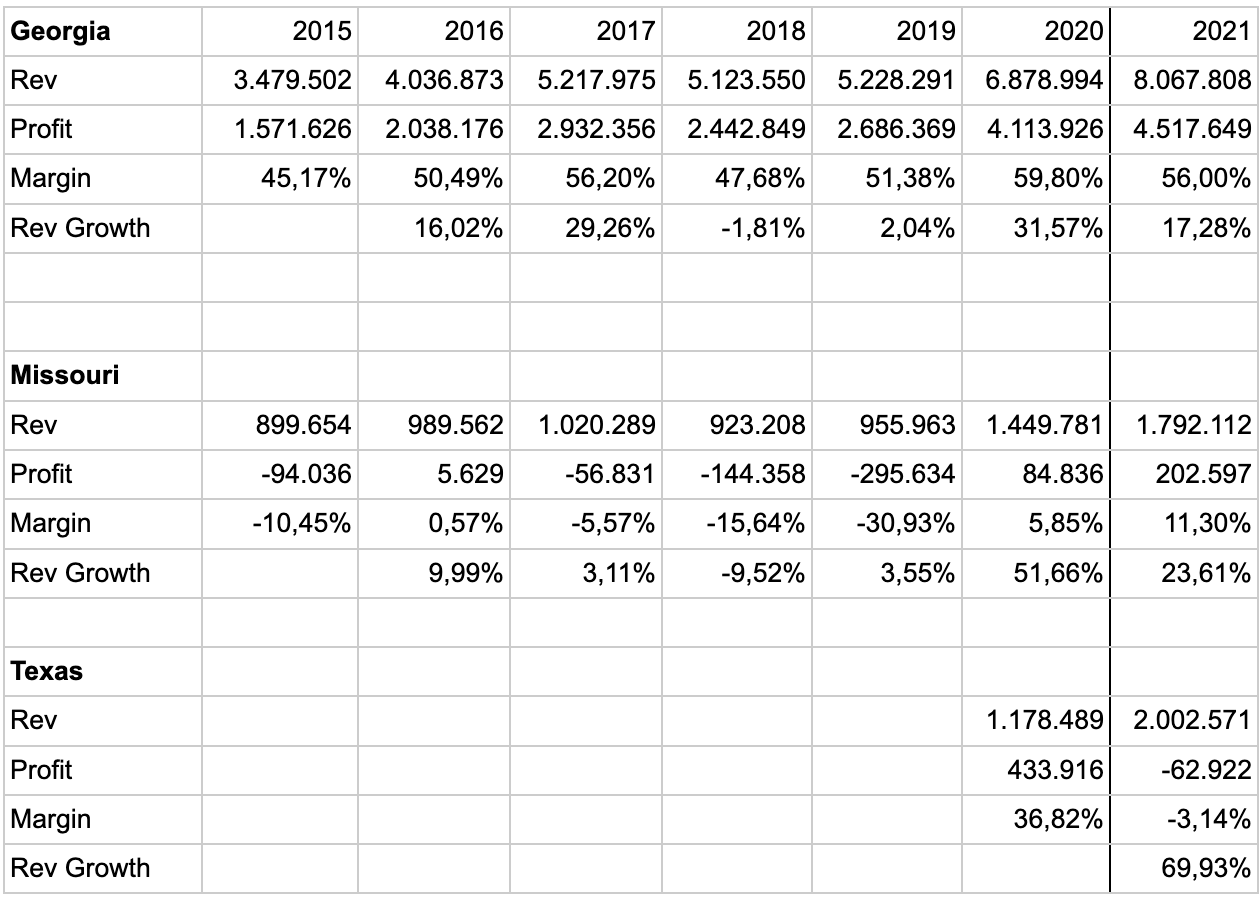

In 2021 Parks! America reported revenue of $11,8 million, an increase of 24,8% from the prior year. Income before taxes has been $3,6 million, an operating margin of 31%.

Since the business is very capital-light, a high percentage of the revenue converts into Free Cash Flow. For 2021 they had $3.3 million in Cash Flow from operation minus $988.000 in Capex equals a free cash flow of $2.3 million for FY2021.

But let‘s take a look at each park:

Georgia park has always been the crown jewel. In 2021 they reported revenues of $8 million and $4,5 million profit from the Georgia park. Operating margin has increased from 45% in 2015 to 59% in 2020 and 56% in 2021. Showing how profitable the right park can be.

The Missouri park was acquired in 2008 by the old management and has been losing money since. However, in 2020 they reported a profit for the first time and could confirm this result in 2021 with a revenue of $1,7 million and a profit of around $202.000.

The newly acquired Texas park generated $2 million in revenue for 2021 with a loss of around $62.000.

How is it possible that one park generates almost 60% operating profit while the one struggles for years to break even?

Well the answer is simple: Location.

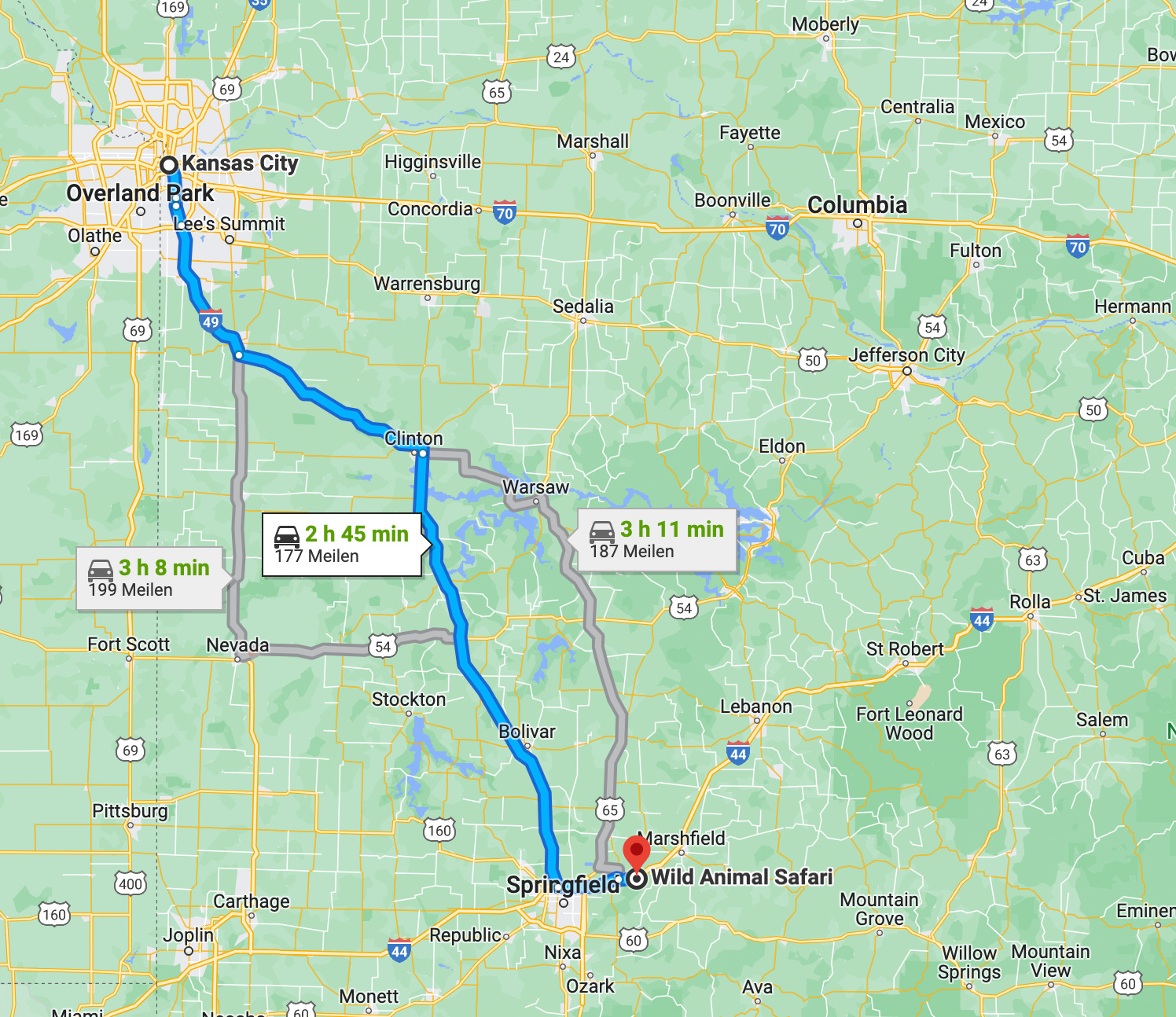

The Missouri park is located near Springfield (Population of around 115.000), Kansas City and St. Louis are the next biggest cities, both are a 2-2.5h car drive away. Around half a million people live in Kansas City and around 300.000 in St.Louis.

The Georgia Park is nearby the Callaway Gardens (an attraction that has 750.000 annual visitors). Besides that, there is also a hiking trail and a water park, all within a 30 min radius. So these attractions drive tourism and a lot of people visit the pine mountains, which comes handy for Georgia Park.

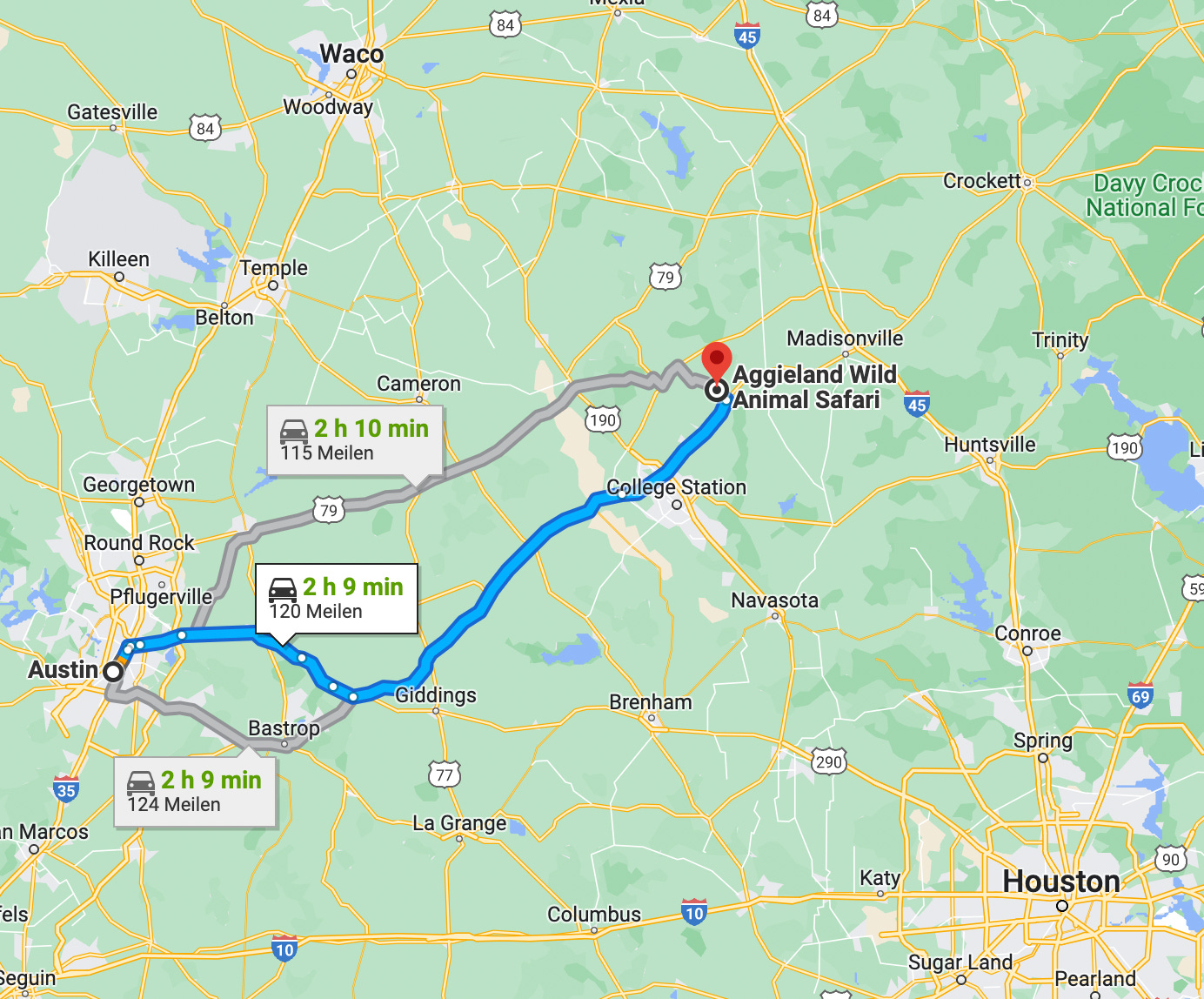

In my opinion, the new Texas Park is not as well located as the Georgia park, but much better than the Missouri Park. Even though there isn't a tourist attraction nearby, the park is close to College Station and a 2h drive away from Houston and Austin.

Furthermore, the weather in Texas is quite good all year long. This is an important factor, which is already shown in the quarter revenues of Aggieland. 21% of the revenue was generated in Q1, Missouri only generated 12% of revenue in Q1.

So, I believe that Texas will become a profitable park.

Valuation:

First this is a very illiquid stock, the share turnover is somewhere between 5-6%. Therefore, most institutions cannot invest in this business. Currently, the company is trading at 3,3 times revenue, 10x EBIT, 14 times Earnings and 17x Free Cash Flow.

I expect that Georgia park will grow at around 8% in the next 5 years, while keeping margins between 58-60%.

Missouri will more or less grow at the same rate, yet with lower operating margin - probably at around 10%.

In addition, I could imagine a 15-20% growth rate for Texas, while increasing operating margins (just like they did at Georgia) to 20-30%.

Given these assumptions, they would generate around 17 million in revenue in 2026 with an operating margin of 40%. It would result in around 7 million in EBIT, applying a multiple of 12 and we get an EV of 84 million, a 100% upside from now.

This valuation does not include another acquisition. After all, I would not be surprised if they did another acquisition in the next 5 years, given the fact that they currently have 6,6 million in cash and generating 2,4 million in free cash flow per year. They stated in their annual report, an increase in Capex for 2022 to generate more revenue, so I expect free cash flow to be a little lower in the next 1-3 years.

What makes this a relative safe bet, is the downside protection.

First they own around 13 million worth of property, second it is a pretty durable business and third if their growth plans fail, they could very well pay out excess cash to shareholders.

Also the valuation and the multiple used above is pretty conservative for a high quality business.

To sum it up, in my opinion Parks! America is an asset-light, highly cash generating, well managed and durable business protected by a local moat trading at a fair price.

Disclaimer: Do not interpret anything above as financial advice. I do hold a position in Parks! America and therefore may be biased. The article was written for entertainment & educational purposes only.

Thank you for that analysis Sebastian! It's a really interesting case and well written. Keep it up!