Q1 Earnings Update - Part II

Profits, pipelines, and a post-mortem

This post concludes the Q1 earnings season. Today we are looking at the earnings from Sanara MedTech (SMTI), Frontera Energy (FEC:TO), Leatt (LEAT), one undisclosed name and one post-mortem analysis.

Sanara MedTech (SMTI)

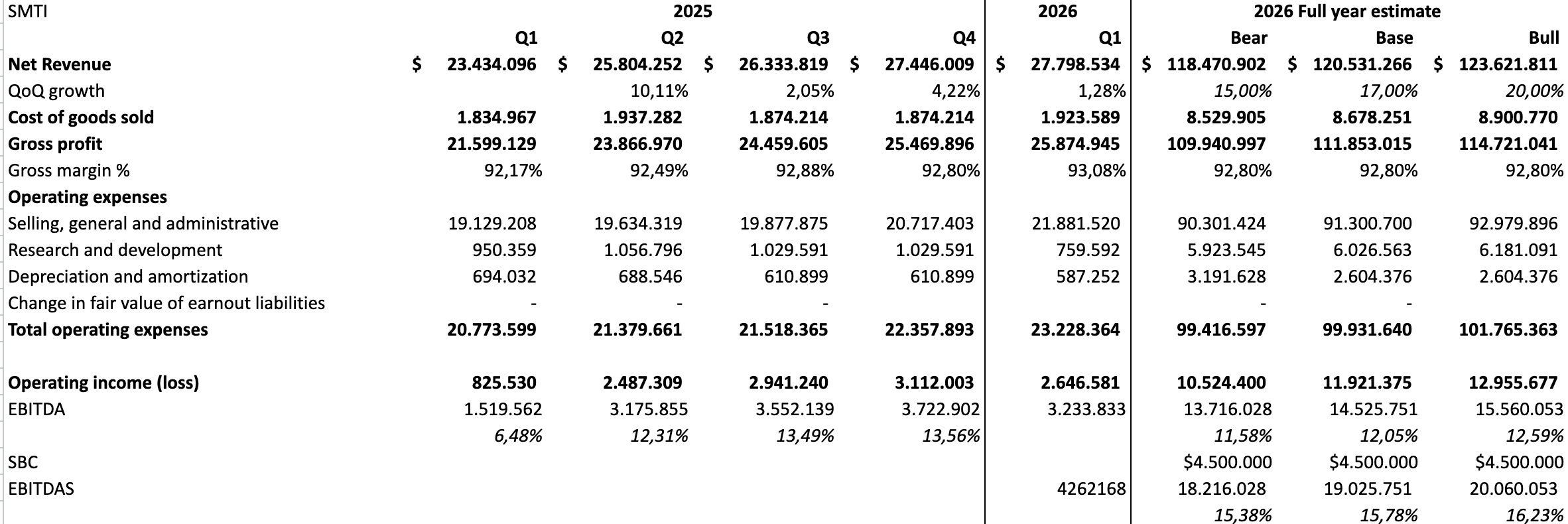

Sanara MedTech had a really strong quarter, in my opinion even stronger than it looked on the surface. While overall revenue grew by 19%, surgical revenue grew by 21%. It was also the first quarter they showed a GAAP profit, despite their still very high interest payments. In my write-up, I outlined the thesis that the company will continue to grow by more than 15%, with multiple growth levers still to pull.

Despite a lower guidance of only 14-17% annual growth, after Q1, I believe the odds are pretty high that they will be able to beat that guidance, as they did this quarter.

Some key KPIs are heading in the right direction: the number of distributors stands at 450+ since Q4, which is 100 more than one year ago. Further, they have hired three additional reps in Q1, who are currently undergoing training and will contribute to sales by the second half of 2026. They did $103M revenue with 40 reps in 2025. $2.5M per rep. Adding three, in theory, could mean an additional $7.5M. As a reminder, the internal reps manage the relationship with the distributors and their 1099 reps who ultimately sell the products to the surgeons.

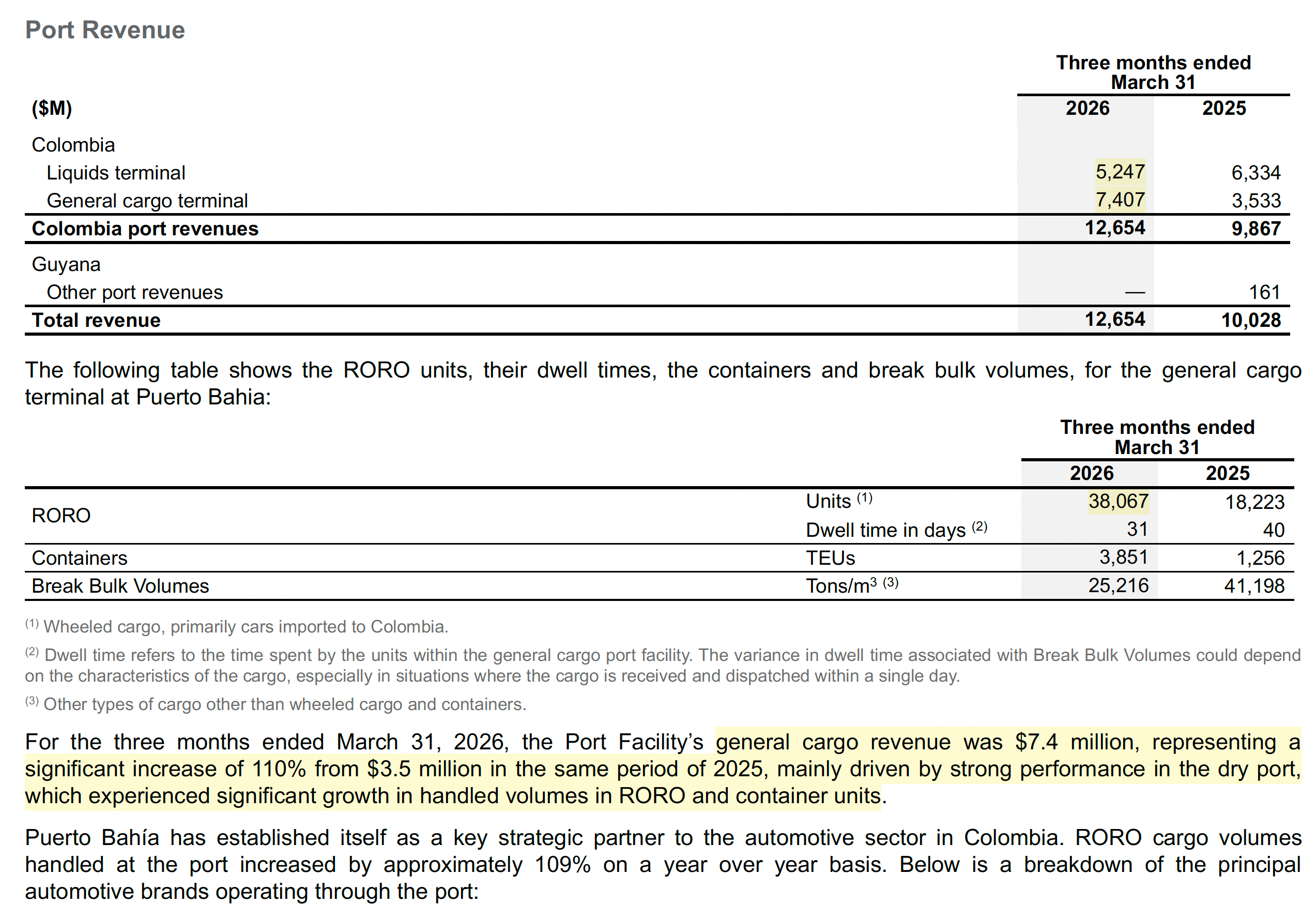

They don't disclose surgeon count growth, but on the call they said “solid growth“ there too.

In January they signed a contract with Vizient, the largest GPO in the States, for BIASURGE. While they don‘t disclose revenue of each product, I believe BIASURGE saw strong growth this quarter, albeit from a small base.

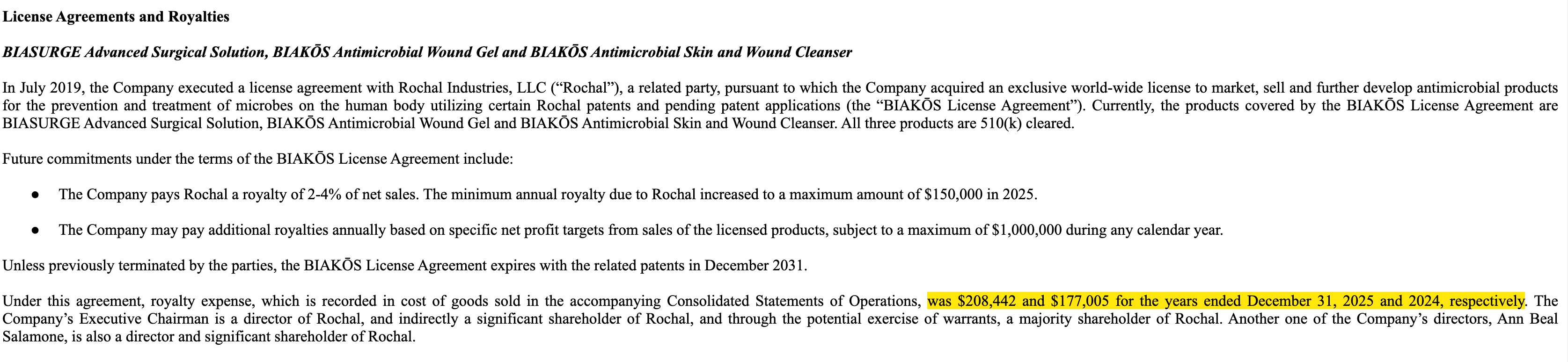

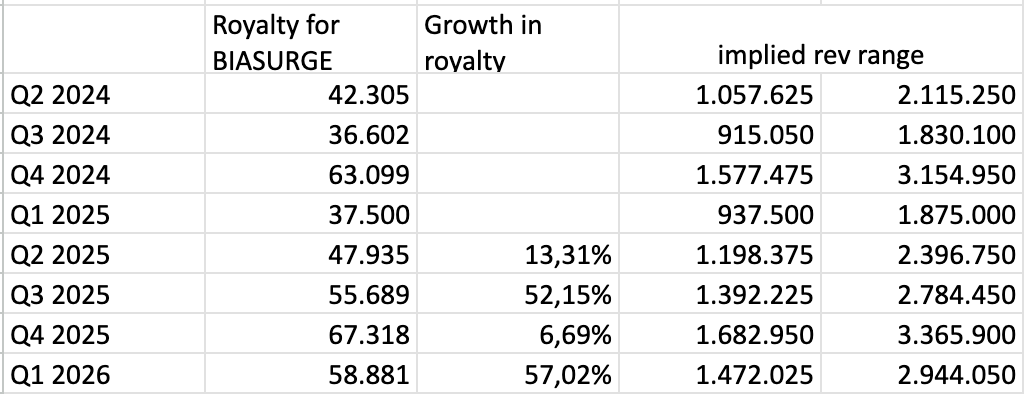

Using the royalty payments for BIASURGE we can estimate a sales range, and also track the growth in royalty payments to get a feel for the growth in BIASURGE.

We have another data point from Q4 2024, where they saw a spike in BIASURGE sales, driven by the hurricane. They disclosed this drove $1.8M in additional BIASURGE sales for that quarter.

Assuming roughly $0.2M of baseline BIASURGE sales at time on top of the $1.8M hurricane spike, that's ~$2M in total BIASURGE revenue for Q4 2024. The $63K royalty payment works out to 3.15% — in line with the 2-4% disclosed range.

In addition, the overall number is not that important, as we know the business is still 80%+ CellerateRX but the growth rate is what matters. And royalty payments grew by 57% YoY this quarter.

It will be an important data point to track as the product gains more traction driven by the new contract and overall adoption.

However, there was also bad news buried in the 10Q, Chemo Mouthpiece did not receive its reimbursement code. Without a reimbursement code it‘s unlikely that the product will get launched. Hence this optionality (it was a joint venture) is likely a 0 now.

”In 2025, CMp applied for a Medicare reimbursement code for its Chemo Mouthpiece oral cryotherapy device, and the application was not approved. CMp has the option to re-apply for the reimbursement code in the future. The Company is evaluating the impact of not receiving approval for Medicare reimbursement and will continue to review this investment quarterly for indicators of impairment.”

- 10-Q, Q1 2026

Overall I am back to my original estimate of 15-20% growth, while I believe 17-20% is the most likely outcome for the full year.

Shares are trading at 1.8x EV/Sales (2026e), which is too cheap in my opinion. The company is profitable, with multiple catalysts still ahead: their refinancing, further ramping of BIASURGE, and the launch of OsStic in 2027

If they can come in at 17-20% growth for the year, I believe the market will start to re-rate shares closer to a 3x EV/Sales multiple.

Frontera Energy (FEC:TO)

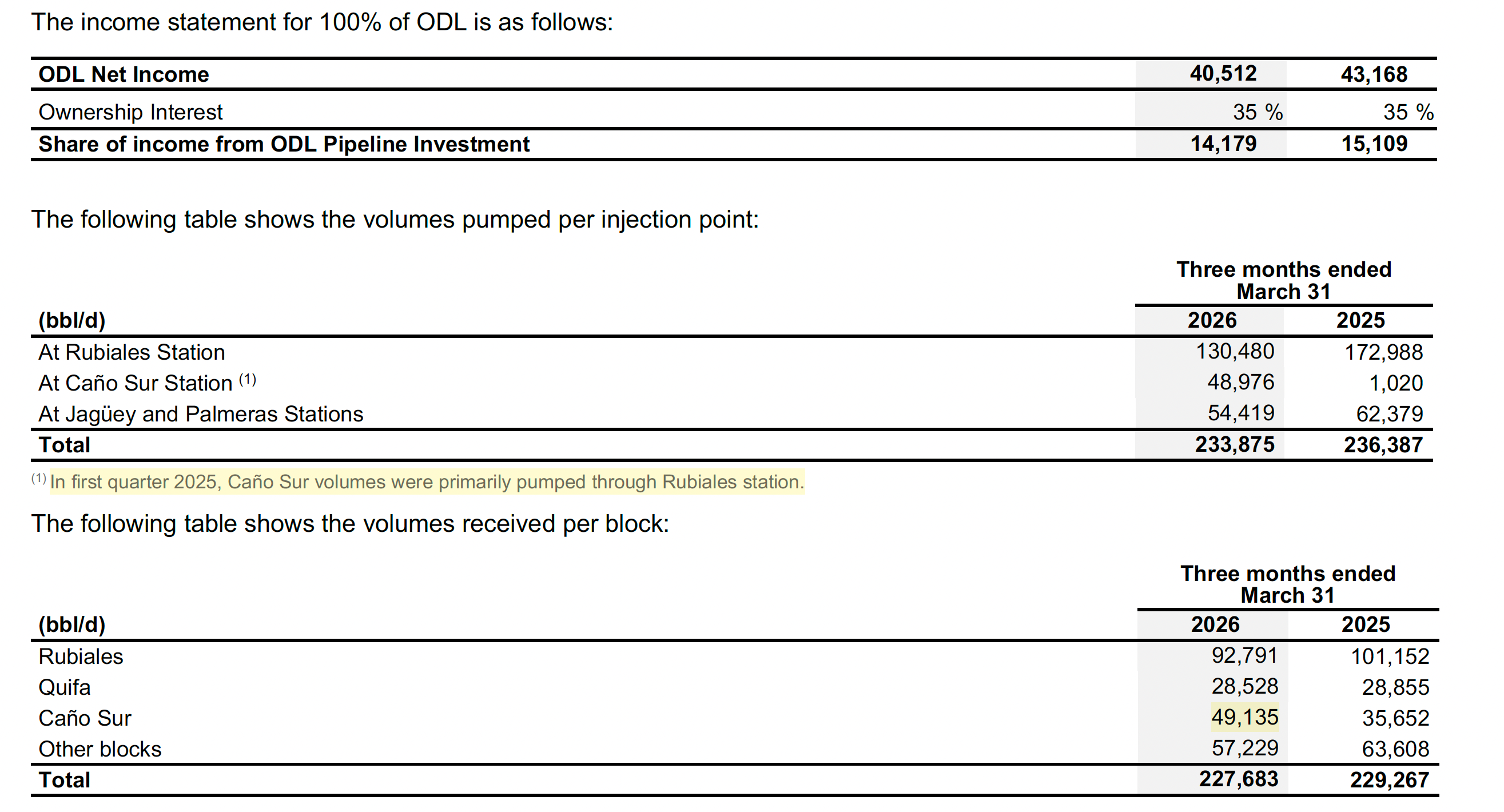

Frontera reported their first quarter as an infrastructure company with the E&P labeled as “discontinued operations”. The infrastructure assets consist of their 35% stake in the ODL pipeline and their 99.7% ownership of Puerto Bahia, a port in Cartagena, Colombia. The dividend payments from ODL can be lumpy and this quarter no dividend was received, which made cashflow appear lower. Regardless, the company expects to receive US$64.7M in dividends from the pipeline this year, 40% in the second quarter, 35% in the third and the remaining 25% in the fourth quarter. The dividend from the pipeline is used to repay their loan via their cash-sweep agreement. This will lower their debt from US$167.8M to US$131M by year end.

Overall the pipeline is a stable source of income, with volumes from Caño Sur offsetting the decline in the other blocks. Caño Sur is one of the growth projects from Ecopetrol.

Applying a 6x multiple to roughly US$65M in dividends net of taxes, would imply a valuation of US$390M for the pipeline alone. Keep this number in mind, as I will show you the current Enterprise value post special dividend.

The port, Puerto Bahia will become the growth engine of the remaining infrastructure stub. It consists of its liquid terminal as well as the general roll-on/roll-off (RORO) terminal. The liquid terminal side is currently declining because they lost one oil trader that stopped doing business in Colombia. General cargo, however, is becoming a real growth driver, increasing revenue by over 100%.

This was driven by the port positioning itself as a key strategic partner for the Colombian automotive sector. Automotive sales in Colombia increased by 26.5% in 2025 and a staggering 47.8% in Q1 2026. This is fueled by imports from (chinese) EVs and a strong peso.

But RORO is not even the real growth story here. Their LPG project started in March 2026, and is expected to reach nameplate by early 2028:

“We also achieved meaningful progress across our energy infrastructure projects, including reaching a key milestone in the LPG project with the successful commencement of initial operations in March 2026, which gives us the capacity to handle up to 10,000 tons per month. We continue making solid progress with the firm goal of becoming fully operational during the first quarter of 2028.”

- Press release Q1 2026

Once the project reaches full capacity it is expected to generate between US$10-15M in EBITDA. Additionally the LNG project with Ecopetrol only needs approval from ANI and is expected to start by the end of this year. This is a critical project for Colombia as it would eventually import 40% of its national demand for natural gas. Frontera is expected to invest $80M in capex to upgrade its facilities.

The project is divided into two phases, the first one with 126 MMcfd , and the full ramp-up would increase throughput to 370 MMcfd from Dec 2028. It is a seven-year take-or-pay contract with Ecopetrol as the commercial partner and responsible for the marketing of the gas, with multiple partners already signed.

Frontera is responsible for the infrastructure and will collect a toll. While the concrete payment is not official yet, talking to other investors and playing around with LLMs gives me range of $0.50-$1/MMBtu. This would imply revenue of US$24M-47M (126 MMcfd × 365 × 1.03 MMBtu/cf = ~47.4M MMBtu/yr → at $0.50 = $24M, at $1.00 = $47M)

Taking $0.50/mmbtu and assuming an EBITDA margin of 70% (which is typical), it would result in roughly US$16M in EBITDA. Adding the US$10M from the LPG project (low-range of the publicly stated guidance) and the current run-rate of $16M it would lead to US$42M in potential earnings power. This does not even include the ramp-up to 370 MMcfd.

Since they have not guided officially yet to anything regarding the project with Ecopetrol, I am not sure whether my estimates are correct, hence I would appreciate anyone with industry expertise to verify them.

Even if I am wrong on the Ecopetrol deal, the current port and the LPG alone provides a path to US$25M+ for the port by 2028. Add whatever you assign to the regasification project on top.

So what is the stock trading at post special dividend?