Ready for Stagflation? Positioning for the Oil Shock — Weekly Treasure Hunt #05

Why the largest supply disruption in history is accelerating the bull case for Latin American energy producers.

I am a bottom-up investor, but ignoring the macro environment is likely as much of a mistake as it is to obsess over it and buy and sell positions based on a tweet from Trump.

Given what is going on in Iran, I think there is a not insignificant chance this will lead to sustained higher prices in oil, fertilizers, and chemicals. I am of the opinion the market has still not really priced in the ongoing war. I may be wrong. This is not a macro call, but I think ignoring it completely is riskier than acknowledging the potential that “something might actually happen” and sizing the portfolio accordingly. What is even more interesting is that most of the effects are just fuelling what the market has been telling us from the start of the year. The sectors that would benefit most from ongoing disruptions are Energy and Chemicals. Both had been the best performing sectors already in January and February, before the war broke out.

Chemicals are a bit more nuanced than Energy, but to give you a sense of how real this already is: roughly 84% of Middle East polyethylene capacity depends on the Strait of Hormuz for export access. Asian petrochemical producers from Japan to Taiwan to South Korea have declared force majeure across the board because they simply can’t get naphtha feedstock.

It all comes down to what your feedstock is. If you’re a producer relying on crude-derived naphtha, your input costs are likely rising more than your output prices. That’s most of Asia and a good chunk of Europe. On the other side, producers using cheap natural gas as feedstock, primarily in North America, become cost-advantaged.

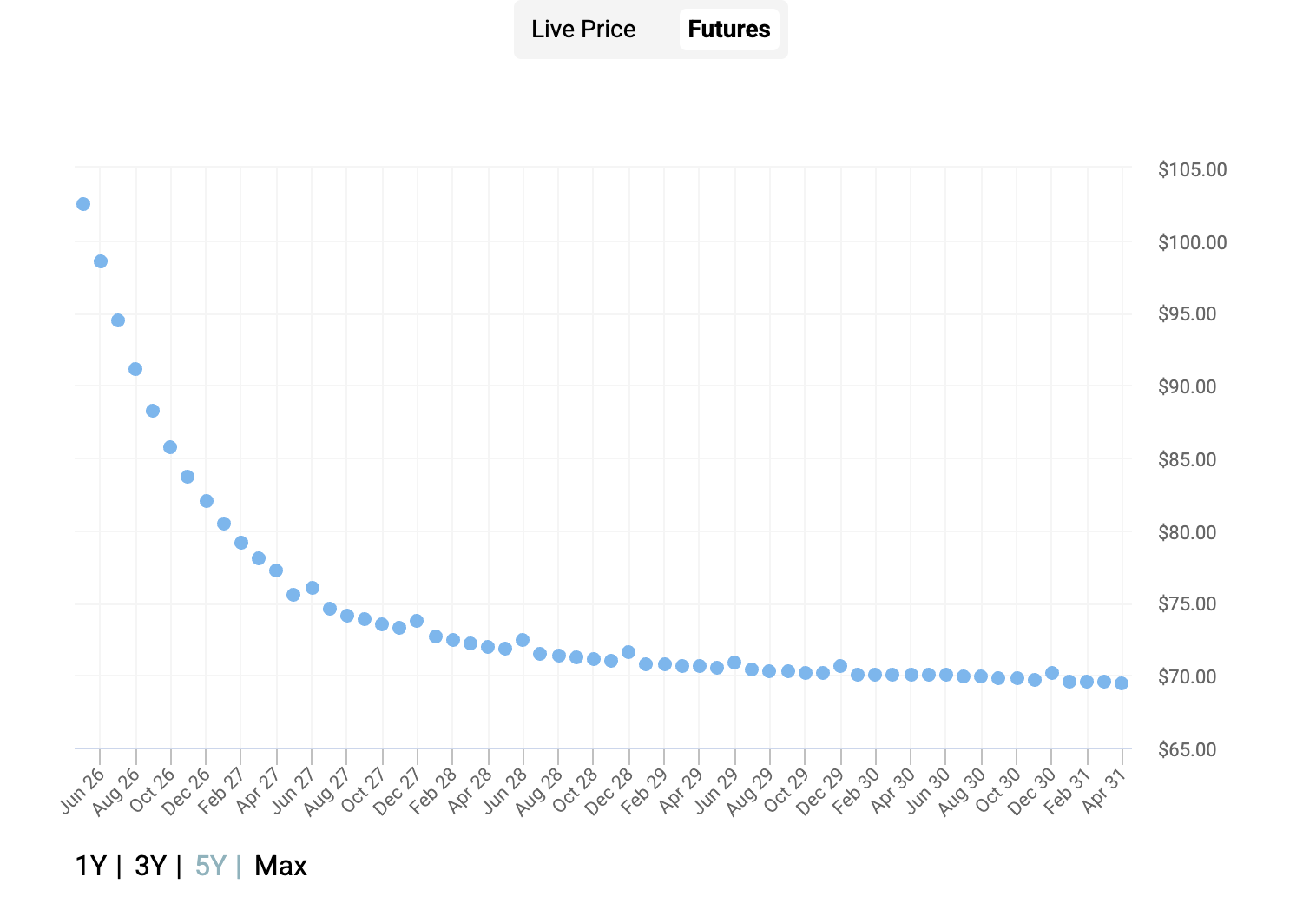

As for oil, futures markets are now pricing in a longer war. While oil prices are still set to decline on the curve, futures are no longer trading below $70 even three years out, and are holding above $75 through May 2027.

And this isn’t just a transit disruption. The IEA’s March report called this the largest supply disruption in the history of the global oil market. Gulf countries have cut production by at least 10 million barrels per day. Physical infrastructure has been hit by drone strikes on terminals in the UAE, Bahrain and Qatar’s Ras Laffan LNG complex. Even Saudi Aramco’s Ras Tanura took damage. You can’t just flip a switch on that. The IEA responded with an emergency release of 400 million barrels, the largest ever, and it barely moves the needle against a ~15 million barrel per day net supply loss.

The important context is that neither $75 nor $100 is actually that expensive, adjusted for inflation. Sure, at the start of the year, some some analysts argued “fair price” might be around $60. But even pre-war, you had very low investment into new fields in the US. Just look up the commentary from McCoy, or any other oilfield service provider, and you’ll get a good understanding of the underinvestment in the onshore Permian.

Quite the opposite is happening south of the border. With higher oil prices, capex spending in Vaca Muerta will only accelerate. “Chevron Eyes Tripling Vaca Muerta Production by 2035”, and VISTA’s CEO has said higher oil prices will likely further increase capex spend there. As a matter of fact, I view Latin America as the potential biggest beneficiary of all of this. I already wrote about cheap Colombian E&Ps here:

And now, one week after the parliamentary elections, we have the first polls, which are looking good.

The way I see the election: Cepeda (left) has his ~35% base of voters. They will always vote for him. The other 65% are undecided, and a good chunk of them will divide between far-right candidate Abelardo de la Espriella and center-right Paloma Valencia. Hence, as the polls are also expecting, the race will likely go into a second round, where I see the likelihood of Valencia winning as not too small. The likelihood, at least, is greater than it was in January. If that happens, Ecopetrol and Parex will be the biggest beneficiaries. Add to that oil prices above $70, and it’s easy to see the potential upside in these names.

Ready for stagflation?

A term that has scared most investors since 2022, and is likely coming back, is stagflation. The comparisons with the 70s were drawn already in 2022, and are naturally returning now. As I already said, my approach is neither to obsess, nor to ignore it, but to attribute a certain likelihood to it actually happening.

As you can see, logically, the best-performing asset classes have been commodities, and interestingly small caps as well. Another potential similarity, albeit a complete long-shot: what was the richest country in South America in the 70s? Venezuela, by a mile. It was one of the 20 richest countries in the world. The ramp-up in Venezuela is taking place right now. Even though it’s still small in absolute terms, it’s happening. Not to an extent that it could offset the 10-20% of lost supply from the Iran war, but enough that it could transform the business of smaller companies.

Maurel et Prom (Disc. I am long) is looking to 3x their production in Venezuela in the coming years.

”Venezuela, -- of course, it’s the big item. We’re looking at more than 400 million barrels in existing reserves at 100%. So of course, we would like to have a strong ramp-up. (…) The ambition is to bring production back up. You may remember this to that 13,000 when we resumed operations, now this then at upwards of 20,000 and we’re looking at 30,000 by year’s end. And our ambition is to reach 60,000 barrels per day by, say, well, within 4 or 5 years.”

— Earnings Call 2025 results

American exceptionalism?

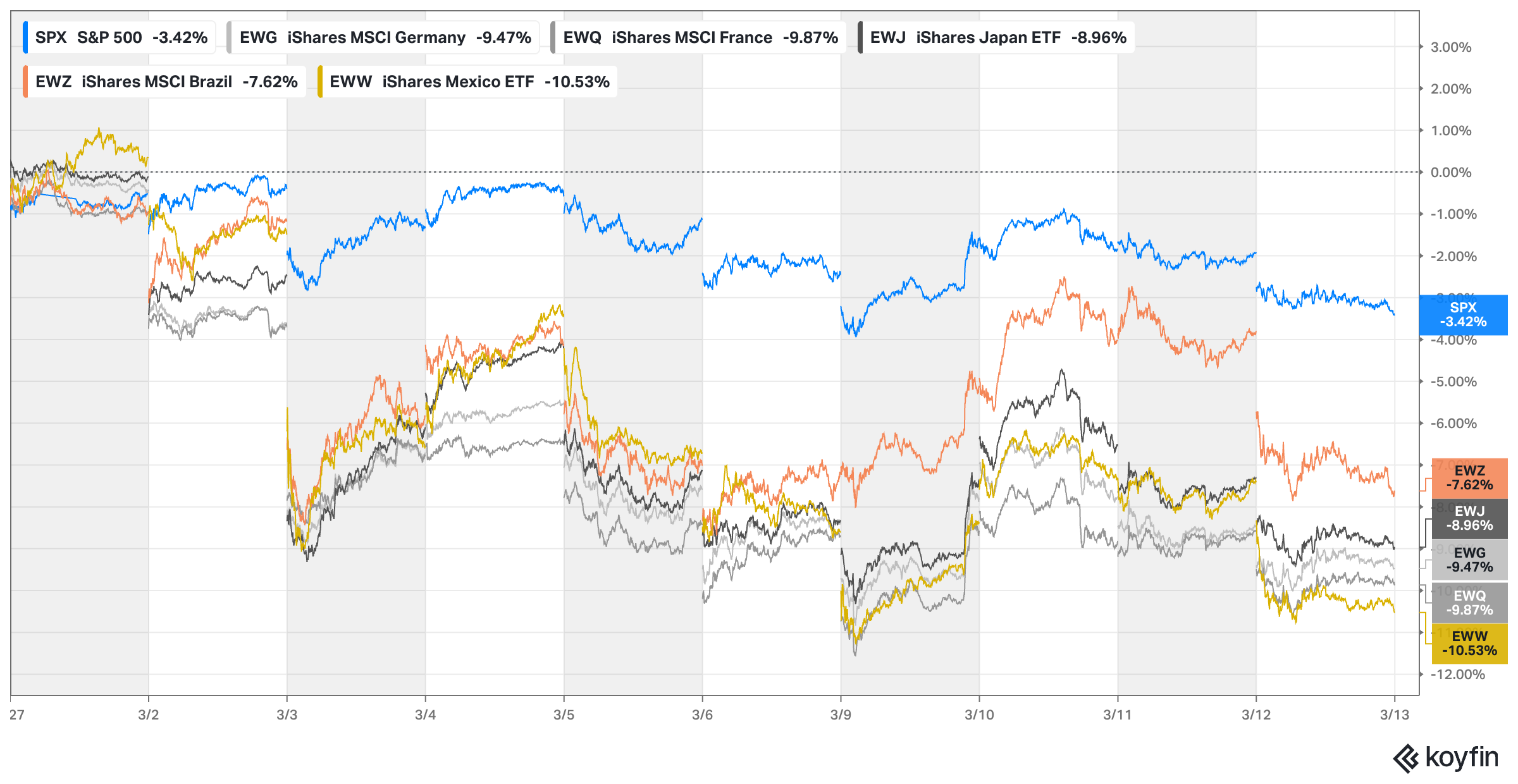

One remaining question mark for me is American exceptionalism. Before the war broke out, it was pretty clear that markets were of the opinion the US is getting weaker while other countries are catching up. The US was lagging all other countries year-to-date, and the dollar had lost roughly 15% of its value compared to the Euro in 2025. However, since the war in Iran broke out, investors have been selling everything to park their cash in USD, and even US stocks. Brazil, for example, lost ≈7% peak-to-trough on the first day after the war. Being up ≈15%+ year-to-date before that doesn’t make this a weak overall performance, but still, since the war, the USD has been strengthening and the S&P has been the best-performing index.

I can totally see why Europe, as a whole, would once again be the big loser of a potential continuation of the war and increasing energy costs. The spread between natural gas prices in Europe and the US has never been higher. Nevertheless, especially in the perception from the outside world, it is fair to say that the US has not gotten stronger with this war. And frankly, the only way out right now seems to be to leave the region without “winning” the war. As a thought exercise, this could potentially be the continuation of the “sell America” trade. Maybe. But then the question remains: what to buy? If energy costs stay elevated, Europe as a whole is not the answer.

I have already described Latin America as a potential destination for capital, especially in an environment of high energy costs. Most of the countries in South America are net energy exporters.

It certainly might be the right time to start hunting outside of the USA.

On this topic, I'd recommend: https://www.biremecapital.com/blog

How to position / trade the current market

As I already outlined, I believe the markets have not really priced in the potential long-term effects of this war. Coming from rich valuations anyway, it would not surprise me to see lower stock prices. I also believe the chances of having higher oil prices for longer are high, because even if the Strait of Hormuz opens, it will take time to recover the production shut-ins. Currently, I have 15% of my book in upstream producers, another 17% in a special situation that recently sold its upstream business and is now a midstream and infrastructure play. Add to that 8% in cash, and I am basically 40% “hedged”, if you will. As of right now, that was a very good decision, and looking at the current market, the only charts that are looking good are the ones from energy-related companies. Importantly, I don’t own them because of the war. I was long most of them before, because of their fundamental progress, but naturally they have become much more attractive relative to other names in the current environment. That, however, may change fast, and I am not married to the thesis. So far, it becomes stronger weekly. If that changes, I will change my mind. But, like it or not, I don’t think you come away in the current market ignoring macro.

Disclaimer: I own shares of Maurel et Prom. I do not own shares in any other company mentioned in this article. Nothing in this newsletter constitutes financial advice, and all content is for informational and entertainment purposes only. I am not a financial advisor. You should always do your own research and consult a qualified professional before making any investment decisions. My positions may change at any time without notice.

smallcaps in a recession? I go with MELI

What about new energy? I’m looking at a New Energy ETF chart right now, and it’s up about 60% over the past year. People seem more inclined to invest in long-term prospects rather than traditional oil companies.